Savings Goals by Age

As your needs and lifestyle evolve over time, so should your savings goals.

3 min read

3 min read

3 min read

Read More

Whether you want to build your emergency fund or save for a down payment, having the right savings account can bring you one step closer to your financial goals. A high-yield savings account is where your deposits can earn a higher interest rate compared to a traditional savings account (hence the name “high-yield”). These accounts are often offered by online banks.

Because you can add and withdraw money with ease, high-yield savings accounts can be a great tool to support any short-term goals you have in mind. Let’s take a closer look at how they work.

High-yield savings accounts work much like a traditional savings account, but they offer a higher interest rate (typically expressed as an annual percentage yield or APY).

A quick refresher on interest: When it comes to savings accounts, interest is the amount of money you earn for leaving your money deposited with a bank. It’s typically expressed as an annual percentage yield (APY), which is the amount of interest you could earn in a year, assuming that funds are not added or withdrawn. The APY also accounts for compound interest. The more often the interest compounds, the more money you could earn.

You can use a high-yield savings account for your everyday savings needs. Once you open an account, you can deposit money as often as you’d like. High-yield savings accounts also offer a great deal of flexibility when it comes to accessing your cash. Generally, you can take out money whenever you want. However, some banks may limit the number of withdrawals you can make each month.

A high-yield savings account is generally considered a safe, accessible place to keep your cash and earn interest. If you’re ready to open an account, make sure that you do so at a FDIC member bank, where deposits are insured up to the maximum allowable by law. Currently, the standard insurance amount is $250,000 per depositor, per FDIC-insured bank, for each account ownership category.

Good to know: If you’re not sure if your bank is a member of the FDIC, you can use the FDIC’s BankFind tool to look up the financial institution and its membership status.

Also, because savings accounts typically have low to no risk and are more liquid than investment accounts, they can be a good place to park any cash you’ll need in the short term (e.g., for an upcoming vacation, holiday purchases, etc.).

You can open high-yield savings account at a variety of financial institutions such as banks or credit unions. To choose the right account for you, it’s a good idea to do a little bit of research and comparison shopping.

Here are a few questions to consider:

Found an account you like? Next step is to open it, which you can do in person or online depending on the bank.

The financial institution will usually ask you for the following:

If the account requires an initial deposit, you can typically fund your account with cash, a check, or wire transfer.

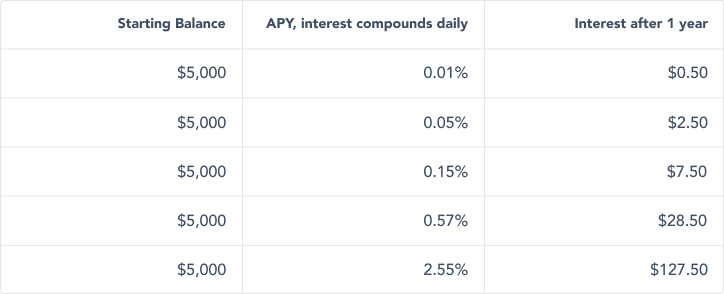

The APYs on some savings accounts might not result in a lot of change to your balance. Check out this chart to see what we’re talking about.

This article is for informational purposes only and is not a substitute for individualized professional advice. Articles on this website were commissioned and approved by Marcus by Goldman Sachs®, but may not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions. Information and opinions expressed in this article are as of the date of this material only and subject to change without notice. You are not permitted to publish, transmit, or otherwise reproduce this information, in whole or in part, in any format without the express written consent of Goldman Sachs. This foregoing restriction includes, without limitation, using, extracting, downloading or retrieving this information, in whole or in part, to train or finetune a machine learning or artificial intelligence system.

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!