Saving vs. Investing: What's the Difference?

Each has an important role to play in helping you meet your financial goals.

4 min read

4 min read

4 min read

Read More

A certificate of deposit or CD is a popular type of deposit account offered by banks. CDs are usually considered low-risk because you get the return of your principal along with any interest accrued at the end of the CD term. Also, if you open an account at a FDIC member bank, your deposit is insured up to the maximum allowable by law, which is currently $250,000 per depositor, per FDIC-insured bank, per ownership category.

CDs can be a great savings tool if you’re looking to earn interest on any extra cash you may have and don’t need to use it for something else in the near term.

In this guide, we’ll cover:

When you open a CD account, you agree to leave your money deposited with the bank for a certain period of time – this is known as the CD term. At the end of the term, you can expect the return of your principal along with any interest accrued during that period.

CDs usually offer a higher interest rate (commonly expressed as an annual percentage yield or APY) than a traditional savings account. The trade-off for the higher interest rate, however, is that your cash may be less accessible: If you withdraw your money before the CD term ends or “matures,” you can expect to pay an early withdrawal penalty (unless it’s a no-penalty CD).

When shopping for a CD account, you’ll notice that banks will offer a variety of APYs and terms. Generally, a CD with a longer term will have a higher APY. For example, a five-year CD will likely offer a higher APY than a 12-month CD.

If you’re looking to open a CD, start by figuring out how much you want to save. Be realistic about how much you’re comfortable putting away. Since your money is going to be tied up for the term, it’s important to choose a CD that makes sense for you and your goals.

When your CD nears its maturity date, you'll have to decide what you want to do with the money in your account.

Be on the lookout for a maturity notice. Your bank is required to send one to you via email or mail before your CD matures. The notice will include the maturity date, and depending on your bank, they may also outline your maturity options. The choice is yours. Generally speaking, you may choose to withdraw your money or put it back into another CD.

When you have excess cash and want to put it to work earning interest, a CD can be a smart option to help boost your savings. You may also have a specific financial goal in mind that you want to save up for – like a dream vacation or home renovation. Or perhaps, you’re simply looking for a place to park some of your cash while the rest remains invested in the market.

Whatever your goals may be, remember: If you’re willing to keep your money deposited for a predetermined amount of time without needing access to it, you could receive a much more competitive interest rate with a CD than you would with a traditional savings account.

And many CDs come with fixed rates. That means once you lock in a rate, you’ll know exactly how much interest you can earn by the end of the term. In other words, you won’t have to worry about rates going up or down.

Look around the web or your preferred bank, and you’ll come across different types of CD accounts. Here are some common ones you may see:

High-yield CDs. These CD accounts offer a higher interest rate compared to traditional CDs. They usually come with a fixed rate, so you’ll know exactly how much interest you’ll earn on your money.

No-penalty CDs. Unlike traditional CDs, no-penalty CDs offer more withdrawal flexibility when you need to access your funds. Generally, you’re allowed to withdraw your money before the end of your CD term without penalty. With a Marcus No-Penalty CD, for example, you can withdraw your full balance beginning seven days after funding. Keep in mind that each bank will have its own rules when it comes to early withdrawals, so review them carefully.

Highlights:

Bump-up CDs. Interest rates can go up or down at any time. This type of CD allows you to request a rate increase for your CD (usually just once) to the current, higher rate offered by your bank. So for instance, if you open a 3-year CD with a 2% APY and a year later, your bank promotes a 3-year CD with a 3.5% APY offer, you can ask your bank to “bump up” your 2% rate to the new 3.5% rate for the rest of your CD term. However, a downside of this type of account is that the initial interest rate offered may be lower than that of typical CDs.

Bottom line: Each type of CD will come with its own features, benefits, terms, and rules. Be sure to review these details carefully before committing to opening an account.

Employing the right CD strategy could help you move the needle on your savings goals. Here are two common strategies to consider.

A CD ladder is when you deposit money into a mix of short-, medium-, and long-term CDs. The goal of CD laddering is to lock in high APYs across multiple CDs instead of lumping all your funds into one CD.

Say you have $25,000 to build a CD ladder that matures in one-year increments. Your CD ladder could look like this:

Highlights:

*Annual Percentage Yield (APY): Stated APYs are for illustrative purposes only and do not necessarily reflect APYs that are currently available.

As each of the shorter-term CDs mature, you can take those funds and deposit them into new longer-term CDs or use the money as you see fit. Many people use a CD ladder strategy to have the option of a steady, periodic cash flow as CDs mature at different dates.

Learn more: How to Build a CD Ladder

With a barbell strategy, you put half of your money into a short-term CD and the other half in a long-term CD. The short-term CD makes up one end of your barbell, and the long-term CD forms the other end. Together, the short-end and long-end of your barbell is designed to help you achieve a higher average yield over time than a traditional savings account.

Here’s a basic example.

Say you want to deposit $10,000 in CDs. Using a barbell strategy, you would put $5,000 into a short-term CD and $5,000 into a long-term CD with the following terms and rates:

*Annual Percentage Yield (APY): Stated APYs are for illustrative purposes only and do not necessarily reflect APYs that are currently available.

At the end of the five years, you will have earned an overall average yield of 2.0% (1.5% + 2.5% / 2). As you can see, the barbell strategy allows you to take advantage of a higher yield (on the long-term CD) while being able to maintain some liquidity (with the short-term CD).

Learn more: A Quick Guide to CD Barbells

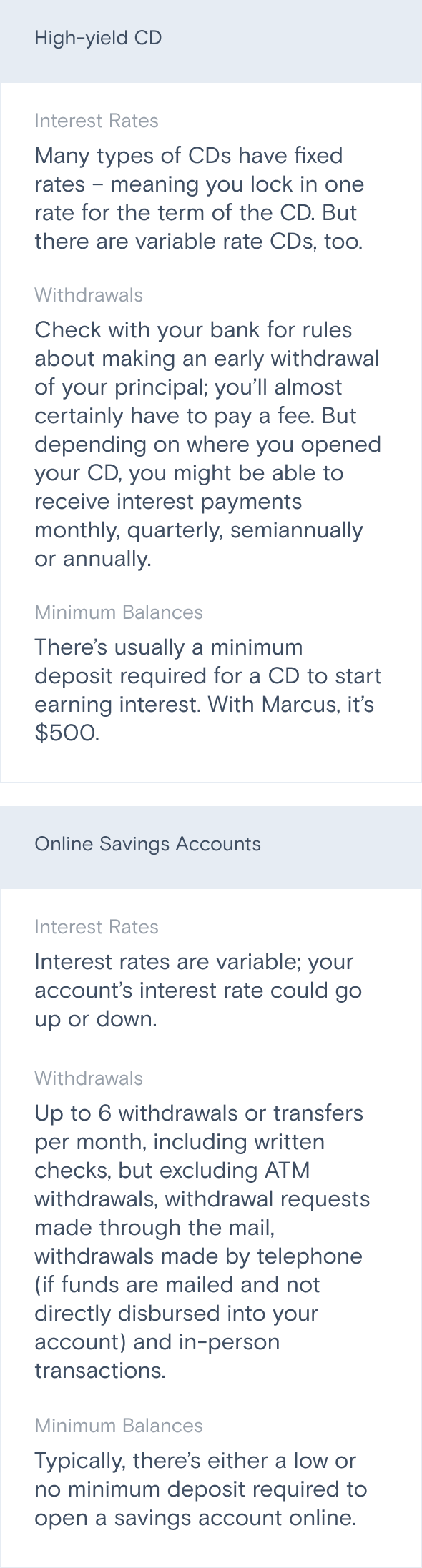

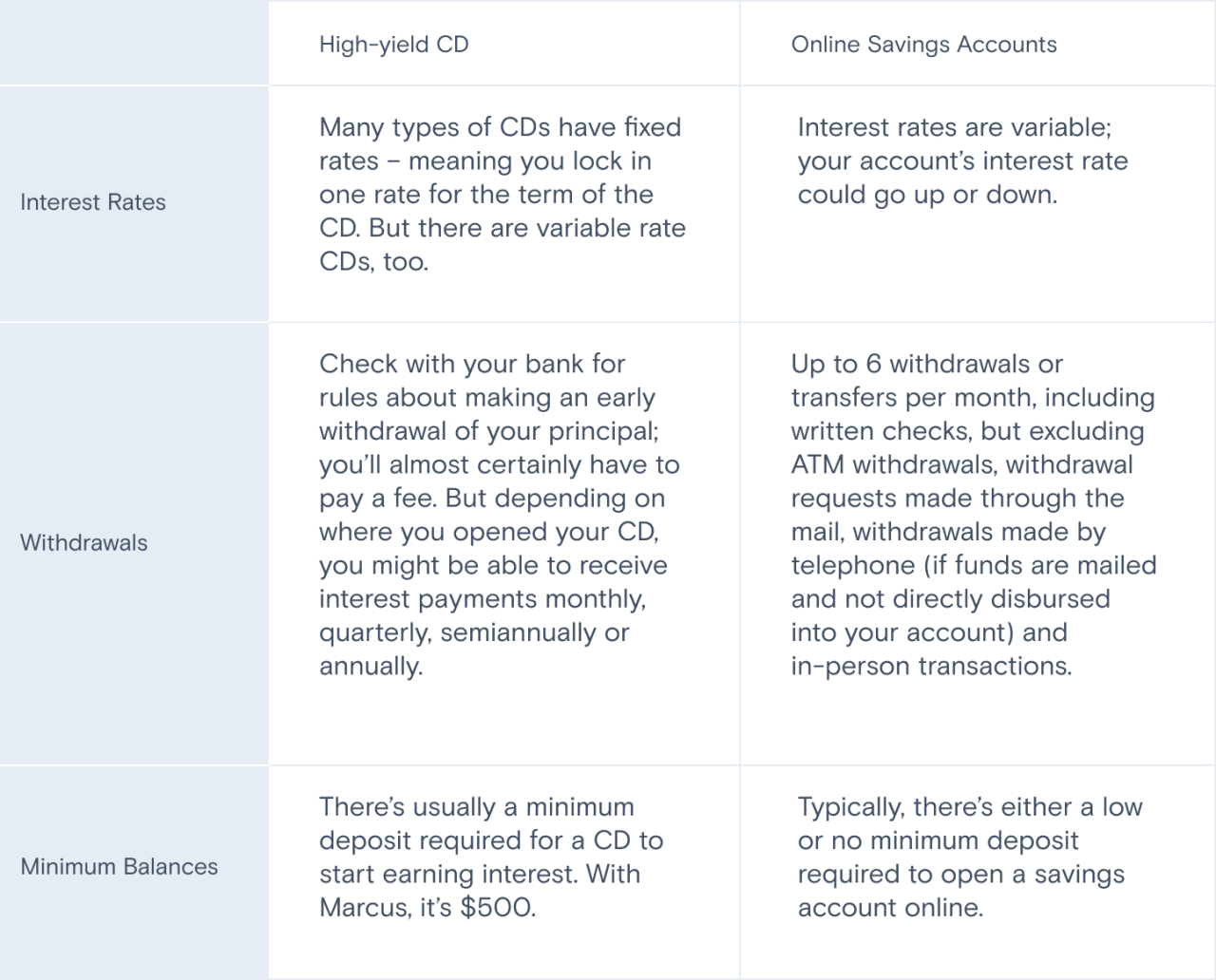

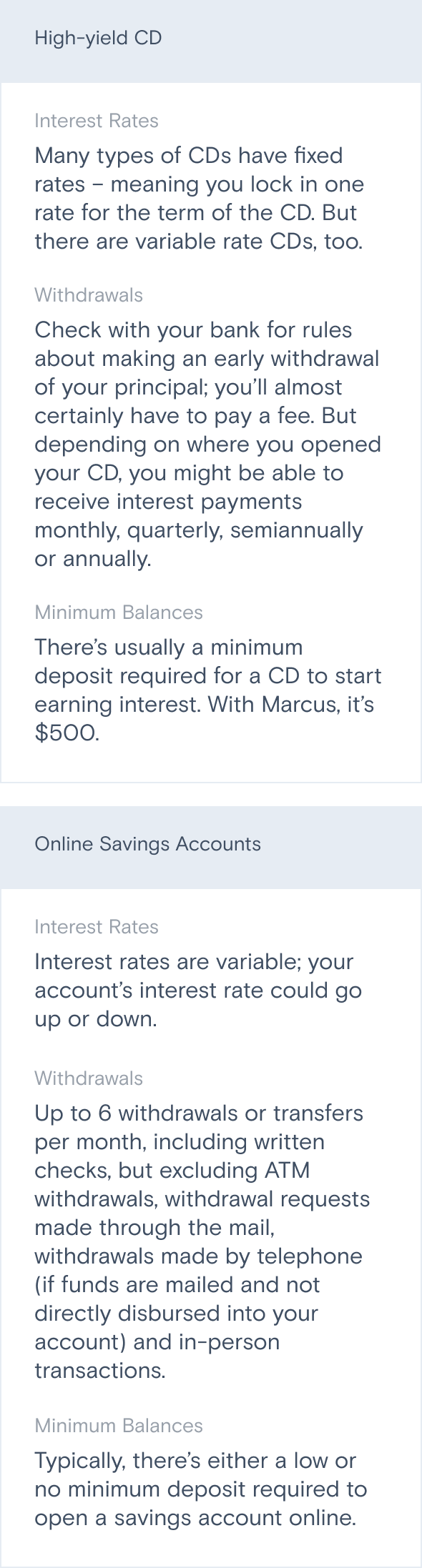

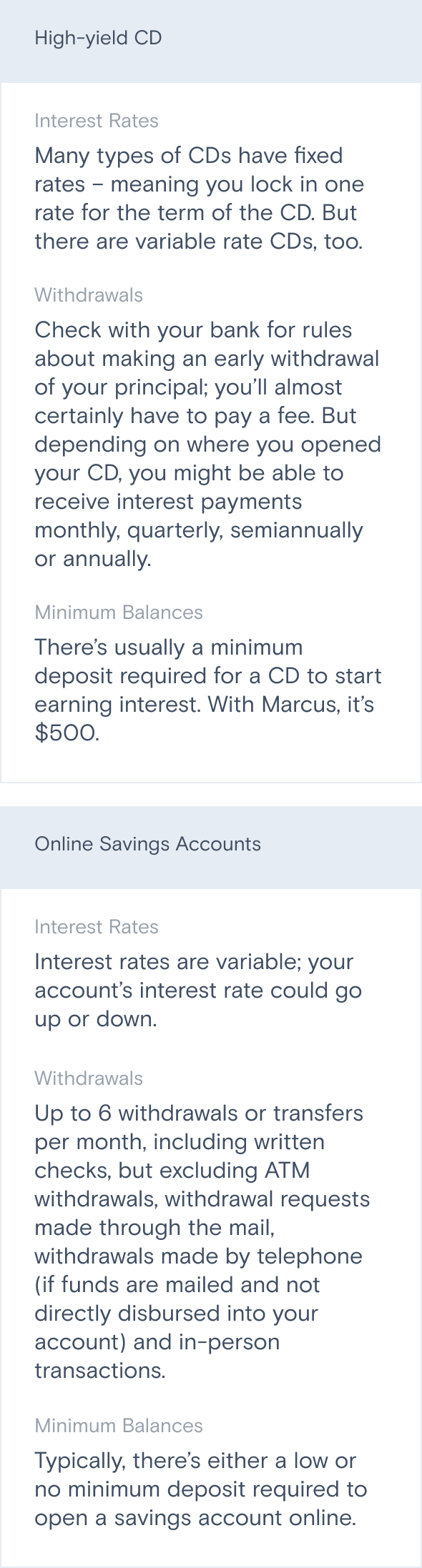

While both are types of deposit accounts that can help you earn interest on your money, they’re not the same. Here are a few key differences.

CD

Online Saving Accounts

|

CD |

Online Saving Accounts |

|

|---|---|---|

|

Interest rates |

Many types of CDs come with fixed rates – meaning you lock in one rate for the term of the CD. But there are variable rate CDs too. |

Interest rates are variable; your account's interest rate could go up or down. |

|

Withdrawals |

Generally, if you withdraw money before the end of your CD term, you’ll have to pay an early withdrawal penalty (unless it’s a no-penalty CD). |

You can take out as little or as much as you want from a savings account. Withdrawals may be limited to 6 per month, depending on your bank and the type of withdrawal you make. |

|

Minimum balances |

There's usually a minimum deposit required for a CD to start earning interest. |

Typically, there's either a low or no minimum deposit required to open a savings account online. |

When you’re ready to open a CD, here are some tips to remember:

Interested to see how much a CD can help your money grow? Check out our calculators: No-Penalty CD Calculator and High-Yield CD Calculator.

Rate:

4.00% APY (fixed)

Access:

Withdraw full balance beginning 7 days after funding.

Fees / Penalties:

No fees, and no early withdrawal penalty beginning 7 days after funding

Min Balance:

$500

Rate:

3.90% APY (fixed)

Access:

Principal amount is locked in until term ends.

Fees / Penalties:

Early withdrawal penalty if you withdraw funds before term ends.

Min Balance:

$500

Annual Percentage Yields (APYs) as of July 28, 2026. Maximum balance limits apply.

No-Penalty CD: APY may change at any time before a No-Penalty CD is opened and funded. Withdrawals permitted beginning seven days after the funding date. $500 minimum to earn stated APY for No-Penalty CD.

Certificate of Deposit: APY may change at any time before CD is opened and funded. Penalties that may reduce CD earnings will apply to a withdrawal of principal prior to maturity. $500 minimum to open a CD and earn stated APY.

This article is for informational purposes only and is not a substitute for individualized professional advice. Articles on this website were commissioned and approved by Marcus by Goldman Sachs®, but may not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions. Information and opinions expressed in this article are as of the date of this material only and subject to change without notice. You are not permitted to publish, transmit, or otherwise reproduce this information, in whole or in part, in any format without the express written consent of Goldman Sachs. This foregoing restriction includes, without limitation, using, extracting, downloading or retrieving this information, in whole or in part, to train or finetune a machine learning or artificial intelligence system.

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!