What Is Home Equity? 3 Key Things to Know

Learn how home equity could help you build wealth over time

4 min read

4 min read

4 min read

Read More

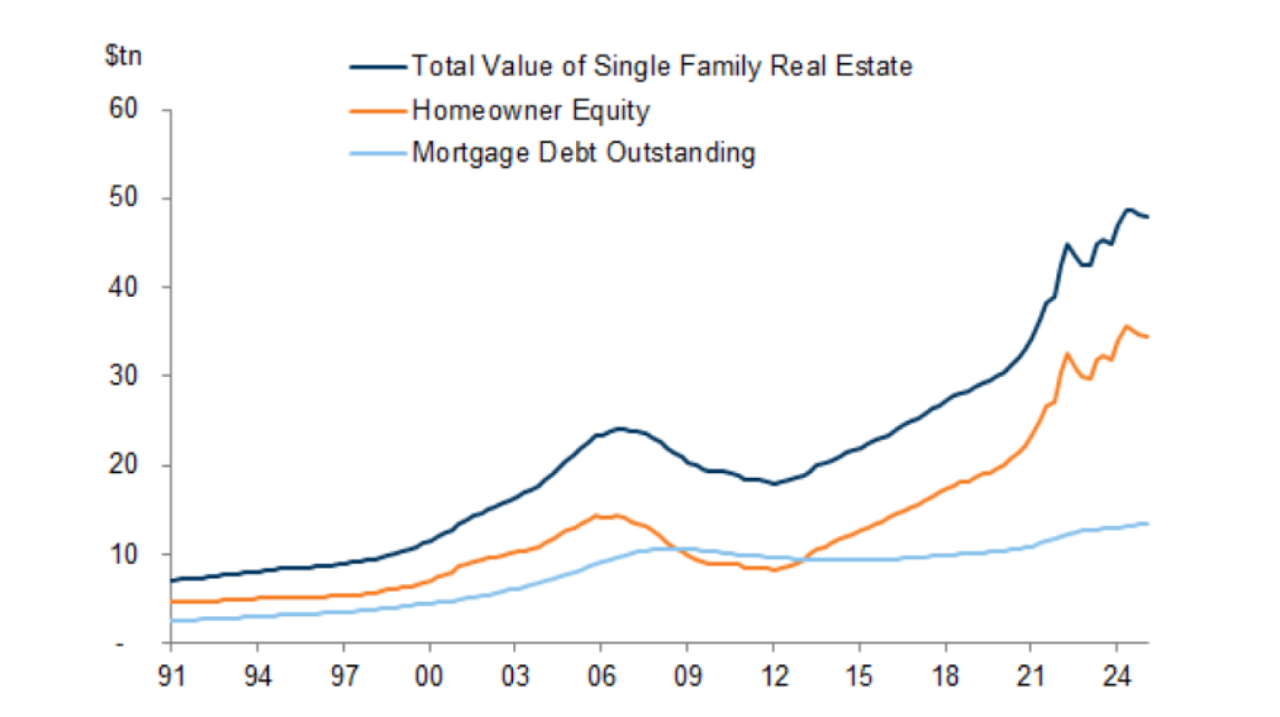

US homeowners are sitting on a sizable amount of home equity—more than $34 trillion according to Goldman Sachs Research. But homeowners aren’t tapping as much into home equity loans, lines of credit, or closed-end second mortgages when compared to the pre-Global Financial Crisis (GFC) era.

Instead, they’re paying down their mortgages in order to own their homes outright. In 2023, 40% of homeowners fully owned their homes, an increase from 2010, when only 33% of homeowners fully owned their homes.

Source: Fed Flow of Funds, Goldman Sachs Global Investment Research

Source: US Census, Goldman Sachs Global Investment Research

Average home prices are one reason why homeowners are staying put.

In January 2020, the median sales price of a new residential home was $329,000. That price has risen to $423,100 in January 2025, according to the US Census Bureau and the Department of Housing and Urban Development.

Retirees who may have wanted to downsize into a smaller home have to consider how the profit may impact their taxes, especially if they are on a fixed income. For younger homeowners who need more space, affordability can be a challenge, as prices climb and they face factors like student debt and a stalling job market.

Generally speaking, the more homeowners stay put, the less inventory there could be, which may drive prices higher.

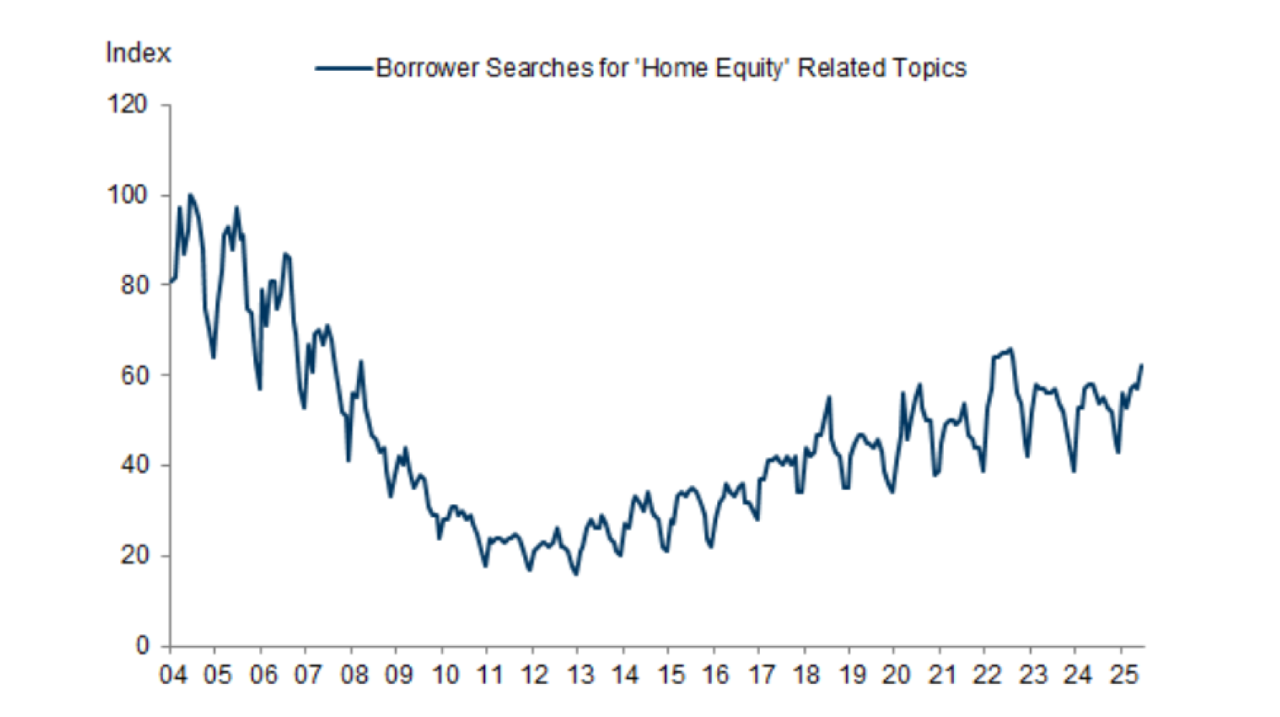

Although there is a considerable amount of untapped home equity, the rate of home equity withdrawal remains slow. And Google searches for home equity—usually a key indicator of interest—have plateaued in recent years.

Goldman Sachs Research believes the continued slow pace of home equity extraction is likely due to higher mortgage rates, stricter underwriting, lower levels of lending, and conservative borrowing behavior.

Note - Numbers represent search interest relative to the highest point on the chart over time. A value of 100 is the peak popularity for the term. A value of 50 means that the term is half as popular.

Source: Google Trends

In 2021, low rates drove cash-out refinancing—homeowners replaced their debt by refinancing and pocketing the difference—but rising mortgage rates have slowed these types of transactions considerably.

Given that 85% of homeowners have loan rates locked in under 5%, higher interest rates make cash-out refinancing less attractive now. Goldman Sachs Research believes that cash-out refinancing activity can start rising once interest rates drop below 6.1%.

Going forward, homeowners and potential homebuyers have a wide variety of issues to consider. Rising inflation, tariff impacts, job market tightening, and overall general uncertainty may inform whether a homeowner stays where they are or feels confident enough to move forward.

This article is for informational purposes only and is not a substitute for individualized professional advice. Articles on this website were commissioned and approved by Marcus by Goldman Sachs®, but may not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions. Information and opinions expressed in this article are as of the date of this material only and subject to change without notice. This article is not a product of Goldman Sachs Global Investment Research. The information contained in this article does not constitute a recommendation from any Goldman Sachs entity to the recipient, and Goldman Sachs is not providing any financial, economic, legal, investment, accounting, or tax advice through this article or to its recipient. Neither Goldman Sachs nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the statements or any information contained in this article and any liability therefore (including in respect of direct, indirect, or consequential loss or damage) is expressly disclaimed. You are not permitted to publish, transmit, or otherwise reproduce this information, in whole or in part, in any format without the express written consent of Goldman Sachs. This foregoing restriction includes, without limitation, using, extracting, downloading or retrieving this information, in whole or in part, to train or finetune a machine learning or artificial intelligence system.

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!

.png)