US Home Prices May Rise as Mortgage Rates Fall

Share this article

Home affordability remains a hot topic as mortgage rates are expected to fall this year.

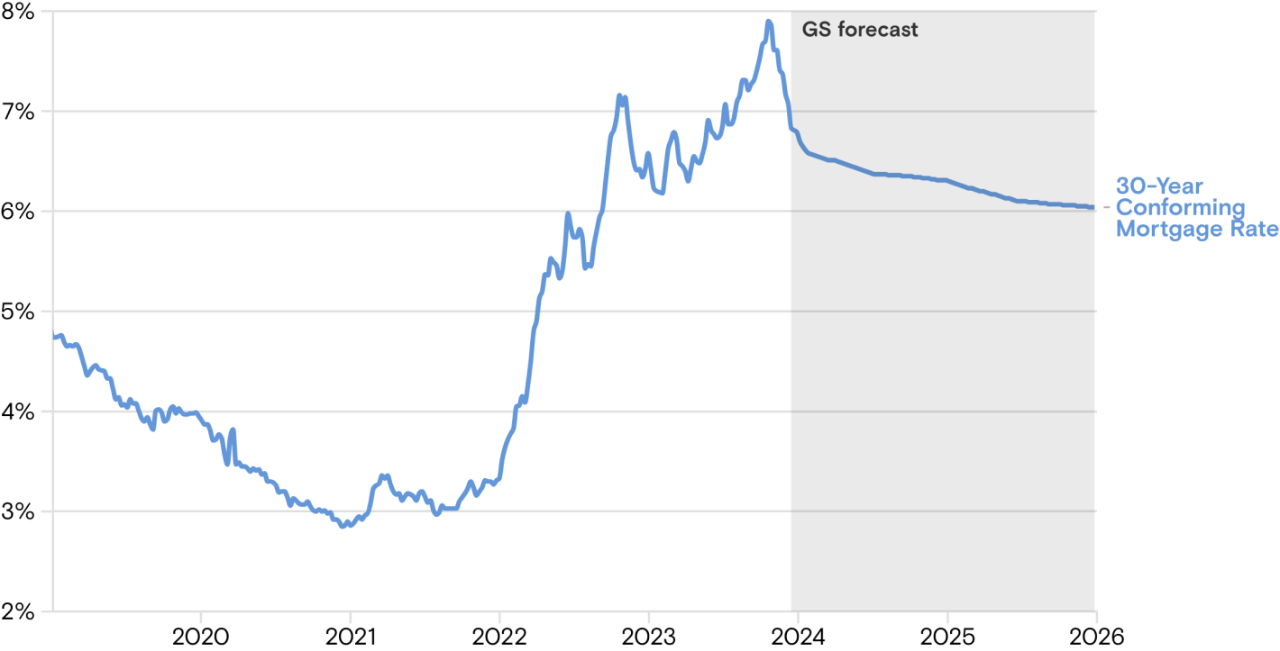

With the Federal Reserve’s anticipated rate cuts on the horizon, Goldman Sachs Research expects 30-year fixed mortgage rates to fall to 6.3% by the end of the year, but US housing prices could increase 5%, a jump from the previous forecast of 1.9%.

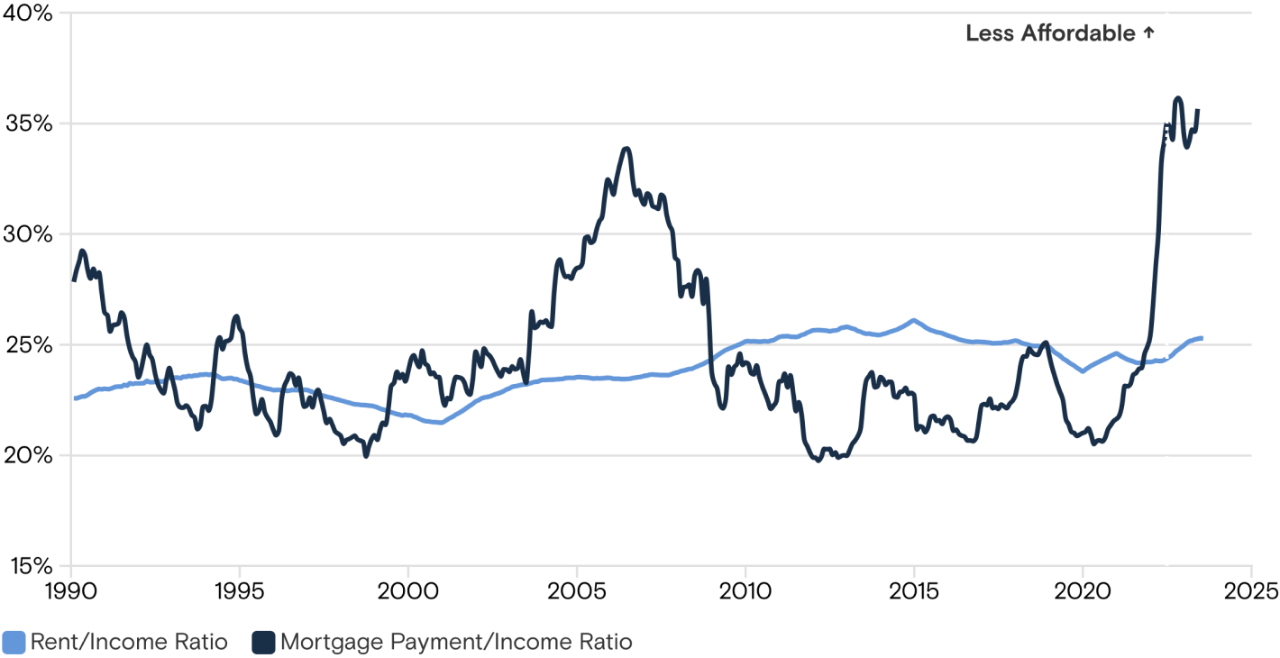

Historically low housing inventory drives part of the forecast, as homeowners don’t have incentive to move out of their current homes when faced with potentially higher mortgage payments. As a result, our Research colleagues find that renting is more affordable than buying even though mortgage affordability may slightly improve in the near term.

Mortgage rates are expected to fall to 6.3% by year-end 2024

30-year conforming mortgage rate with GS forecast

Source: Freddie Mac, Goldman Sachs Research

Goldman Sachs sat down with Research’s Roger Ashworth, senior strategist on the structured credit team, and analyst Vinay Viswanathan to discuss the US housing market and their expectations for the year.

This interview was originally published by Goldman Sachs Intelligence, a series featuring insights on diverse topics of impact within this dynamic economic environment.

Goldman Sachs Intelligence: What are the factors behind your forecasts for faster US home price appreciation?

Ashworth: We pulled forward a lot of the future home price appreciation we expect this year from next year. Some of that is predicated on the broader macroeconomic projections coming out of Goldman Sachs Chief Economist Jan Hatzius’ team. They expect the Fed to start cutting rates in May. We’re now expecting the 30-year fixed mortgage rate to drop to 6.3% by the end of this year. So that’s one factor.

Goldman Sachs Intelligence: What else is going on?

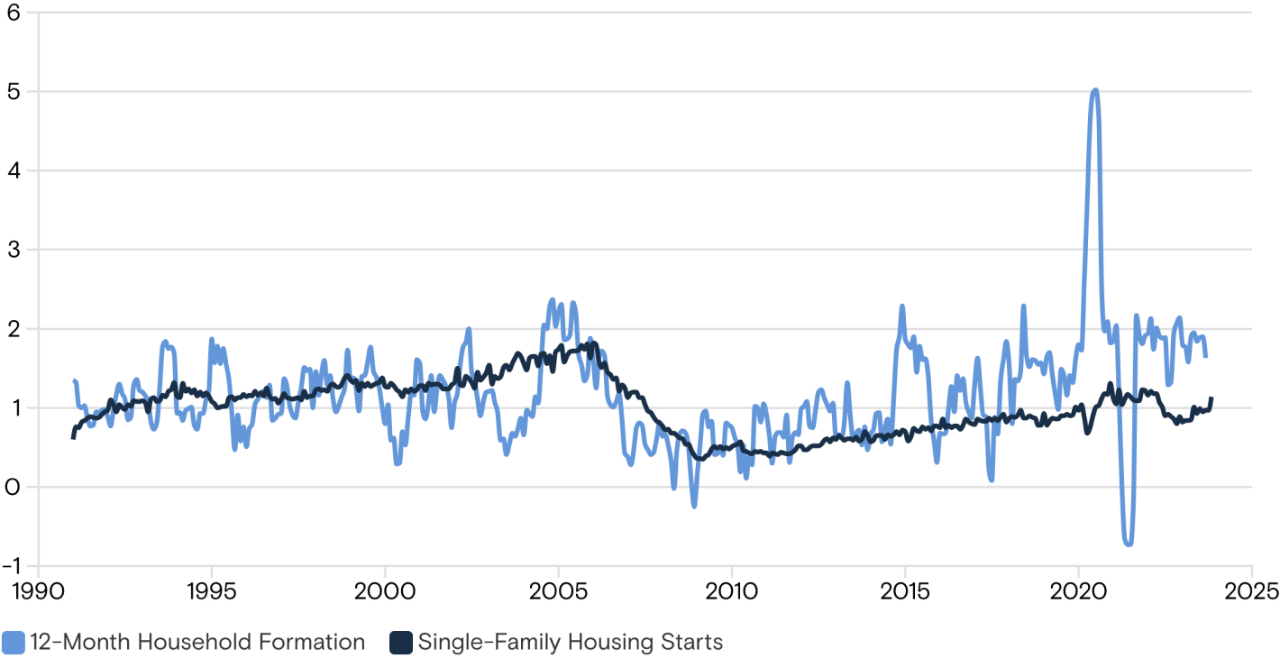

Ashworth: If you look at the more recent home price index releases, the momentum has been pretty high heading into this year. The annualized rate was running around 8% until this month. We have very low inventory of houses for sale, which is generally supportive of prices, along with generally stable demand that is coming from things like household formation.

Goldman Sachs Intelligence: In your research note, you highlight some of the high-frequency data points that have looked encouraging of late. Can you talk about those?

Viswanathan: Taking a quick step back, what we forecast is the Case-Shiller home price index, which is a really robust and widely quoted gauge of home prices. But the issue with the index is it’s a monthly data point, and it can be quite lagged.

For that reason, we also took into account sources such as Redfin, one of the online housing brokerages, which releases weekly data on the median sales price that they see in their system. And in December, the index they maintain was up by 2% on a non-seasonally adjusted basis, which is a pretty substantial increase given the base level of interest rates we had in the fourth quarter. In addition, mortgage purchase applications have stepped up a bit with the drop -in rates. While the level of those applications is still quite low, it’s a forward-looking indicator.

Ashworth: We also look at the Goldman Sachs Financial Conditions Index, which isn’t just reflective of Federal Reserve policy but also borrowing rates in the broader economy. We saw a material, pretty significant loosening of financial conditions as borrowing costs dropped into year-end.

Goldman Sachs Intelligence: You note that inventories remain historically low. Is that primarily a function of current mortgage rates?

Ashworth: Yes, that’s the whole lock-in effect. Everyone refinanced back when rates were at historic lows. If you look at the agency mortgage-backed securities market, which is the lion’s share of overall mortgages outstanding, the average mortgage rate is around 3.9%. Last time I checked, we’re now seeing mortgage rates in the mid-to-high sixes. The incentive for someone to move is quite low as a result, because if you buy the same house down the street, your mortgage payments are going to be significantly higher.

Viswanathan: That’s the main story on the existing side of housing inventory. But there’s also new inventory that typically is roughly 15% of the overall inventory. And, partly because of supply chain issues and labor availability issues, actual completions of new single-family homes have been quite low. So in addition to the locked-up existing market, you’re also not seeing much new supply coming to the market.

Household formation has exceeded single-family home construction

Year-over-year household formation and single-family houses starts (millions)

Source: Census Bureau, Goldman Sachs Research

Goldman Sachs Intelligence: What are you seeing on a regional basis?

Viswanathan: Something that differentiates us from other banks is that our home price forecasts aren’t based on a national model. They’re based on different models that incorporate the largest 380 metros, and then we roll them up into one national number. So we are always cognizant of the local nature of housing.

We see housing falling into three main buckets. There are areas that were expensive and have gotten more expensive, like California and the Pacific Northwest. There are areas that were affordable and have gotten somewhat expensive, like the Southeast. And then there are areas that were cheap and are still relatively cheap, like parts of the Mid-Atlantic and the Midwest. We are the most bullish on the last group. We think the weakest markets will be in California and the Southwest. The Southeast is a bit more confusing. Affordability has gotten much worse, but there are still booming local economies and good migration trends over the past couple of years.

Goldman Sachs Intelligence: How does rental affordability factor into the housing equation?

Ashworth: The largest demographic in the US is 30- to 39-year-olds, and it’s going to continue to grow for the next several years. That’s when life events start to happen in terms of having kids, for example. Some of those people will be making the decision to buy regardless of how rental affordability compares, but it definitely still factors in. With financing costs that much higher right now, it’s still cheaper to rent than to buy. And we believe mortgage affordability will only slightly improve in the near term under our baseline housing and mortgage forecasts.

Rental affordability is superior to mortgage affordability but is strained nonetheless

Housing vs. Rental Affordability Indexes

Source: Goldman Sachs Research

Goldman Sachs Intelligence: What are some of the key risks to your outlook?

Ashworth: There is a risk that the market went too low on its rate expectations late last year and that the Fed doesn’t deliver on rate cuts. If inflation remains relatively high, that adds extra cost to the consumer. And if income growth doesn’t show up and keep pace with inflation, that would hurt affordability.

The other thing we’re watching is the labor market. There has been some loosening there, but the labor market remains quite tight relative to history. We haven’t seen much in the way of job losses, which has kept the foreclosure rate relatively low. A pickup in job losses would not only cause US consumers to lose confidence and put off home purchases, it would also cause distressed sales and foreclosures to rise, putting downward pressure on home prices.

This article is for informational purposes only and is not a substitute for individualized professional advice. Articles on this website were commissioned and approved by Marcus by Goldman Sachs®, but may not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions.

Related Content

4 min read

4 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!