A New Kind of Recession?

Share this article

These insights were originally published by our colleagues at Goldman Sachs Asset Management as part of their GSAM Connect column.

It’s human nature to want to classify and label observations. Whether the classification is large or small, red or blue, round or square, it can help provide structure and context to decision-making. But what happens when what we’re observing is actually medium purple trapezoidal? Strict classifications can sometimes fail to accurately describe what we’re seeing.

In the US, the official arbiter of the economic cycle is the National Bureau of Economic Research (NBER). NBER says a recession involves a significant decline in economic activity that is spread across the economy and lasts more than a few months. The macroeconomic debate has centered on the likelihood of a hard landing (recession) or soft landing (Fed succeeds in controlling inflation without a recession).

Many observers in the recession or hard-landing camp point to the inverted yield curve, an aggressive Federal Reserve reaction function, and depressed leading indicators to validate their recessionary expectations.

On the other hand, those who believe in a soft landing cite labor market strength, robust private sector wealth and spending, growing real income, and the absence of systemically hefty bubbles as signposts to a narrow path for recovery, in which growth may dip below trend to help resolve macroeconomic disequilibrium but doesn’t descend to recessionary levels.

While both hard- and soft-landing camps are academically confident, maybe the actual economic outcome lies somewhere in between...a rolling recession.

As the US economy has evolved from a heavy industrial to a service and financial economy, impacts on the business cycle, inflation and monetary policy have become uneven. So, instead of having a simultaneous and comprehensive downturn, or completely avoiding a contraction, we’re seeing a staggered response to shifting dynamics such as tighter financial conditions, higher cost of capital, and inflation.

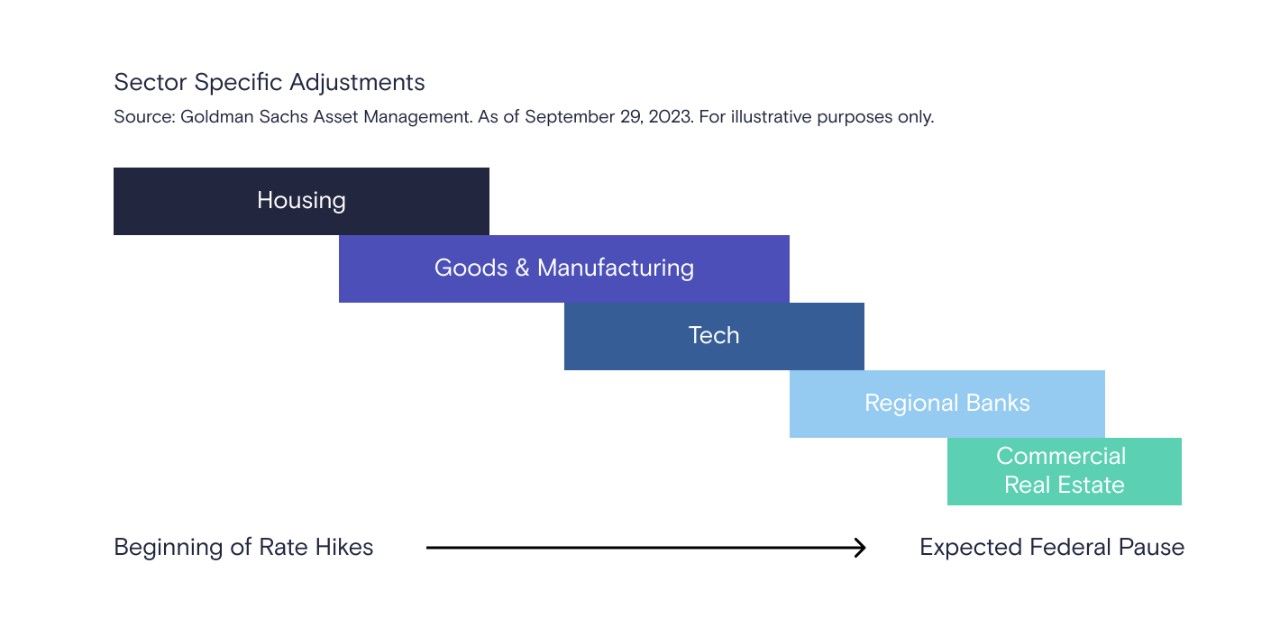

In the current economic cycle, we can observe a cascading series of sector adjustments. In early 2022, housing, the most rate-sensitive part of the US economy, experienced a major downturn in demand as mortgage rates spiked. Many in the mortgage industry would say housing has already gone through and exited a recession.

Later in 2022, the consumer sector experienced pockets of inventory glut as consumption patterns shifted from goods to services just as the supply chain was recovering. Heavy price cutting and margin pressure followed. Shortly after, the elevated cost of capital began to weigh on the information technology sector, which had overexpanded during the work-from-home surge. Layoffs became common, but many displaced workers found new jobs relatively quickly. Then tech passed the baton. Today, commercial real estate is having its turn.

There is clearly a common economic thread across these sectors. But their adjustments have been idiosyncratic and the rebalancing of these industries doesn’t seem systemically large enough to contaminate the broader economy.

To be sure, many sectors are also thriving. We see tremendous resiliency across travel and leisure, healthcare, artificial intelligence, multi-family housing, and commercial industrial and storage real estate, to name a few.

Whether it’s a hard or a soft landing of the economy, a recession may be the most widely anticipated nonevent since the Y2K problem. But instead of viewing the data as unclear, it seems more likely it just doesn’t fit with traditional economic classifications, and a rolling recession is a more accurate description of current conditions.

This article is for informational purposes only and is not a substitute for individualized professional advice. Articles on this website were commissioned and approved by Marcus by Goldman Sachs®, but may not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions.

Related Content

3 min read

3 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!