Guide to Savings Accounts

April 4, 2024

Share this article

Banks and credit unions offer a variety of savings accounts. No matter what you’re trying to save up for, it’s important to understand how different types of accounts work and how they could work together to help you reach your savings goals.

In this guide, we’ll review the basics and go over a few popular types of savings accounts you’ll likely come across in the market.

What we’ll cover

What is a savings account and how do they work?

Next to piggy banks, a savings account may be the most common place to keep your cash. You can deposit money, earn interest, and make withdrawals. Traditional and high-yield savings accounts typically require a low minimum opening deposit to set up an account.

Once you open an account, you can deposit money as often as you’d like. Many banks offer a recurring deposit or transfer feature that can help you automate your savings.

Savings accounts can offer a great deal of flexibility when it comes to withdrawals too. Generally, you can take out money whenever you want. But be aware that some banks may limit the number of withdrawals you can make each month depending on the type of withdrawal you make. If you’re unsure about your account rules, contact your bank directly for more information.

Learn more: What Is a High-Yield Savings Account?

Are savings accounts safe?

Savings accounts are generally considered a safe, accessible place to keep your cash and earn interest. When shopping for an account, it’s important to look for a FDIC member bank, where deposits are insured up to the maximum allowable by law. Currently, the standard amount is $250,000 per depositor, per FDIC-insured bank, for each account ownership category.

If you’re not sure if a bank is a member of the FDIC, you can use the FDIC’s BankFind tool to look up the financial institution and its membership status.

Because savings accounts typically have low to no risk and are more liquid than investment accounts, they can be a useful place to park your money for short-term goals like an emergency fund or a down payment.

Learn more: What’s the Difference Between Saving and Investing?

Reaching your goals starts with saving for it. See how Marcus could help.

Key features to consider when opening a savings account

Not all savings accounts offer the same features. Here are a few things you’ll want to pay attention to:

Annual Percentage Yield (APY). This is the amount of interest you could expect to earn if you leave your money deposited in a savings account in a 12-month period. Be aware that the APY on traditional or high-yield savings accounts is variable, which means it can go up or down.

When comparing your savings account options, take a look at the APY to see if you’re getting a competitive rate. Even small differences in APYs could make an impact when it comes to how much you earn on your savings. Check out our savings interest calculator to see how interest could add up over time.

Good to know: You’ll likely find that online banks may offer more competitive APYs than traditional banks.

Annual Percentage Yield (APY) as of April 23, 2024. APY may change at any time before or after account is opened. Maximum balance limits apply.

This calculator is for illustrative purposes only and may not apply to your individual circumstances. Calculated values assume that principal and interest remain on deposit and are rounded to the nearest dollar. All APYS are subject to change.

Rates of the selected banks reflect New York savings rates for similar products at the select banks with a minimum balance of $2,500. Rates may vary by state and do not account for bonus, special or promotional APYs. National Average is based on the APY average for high yield savings accounts with a minimum balance of at least $2,500 offered by the top 50 US banks (ranked by total deposits). Rates of selected banks and the National Average as reported by Informa Financial Intelligence, www.informars.com. Informa has obtained the data from the various financial institutions that its tracks and its accuracy cannot be guaranteed. This calculator does not include all savings accounts available in the marketplace.

Our rate as of April 23, 2024.

Comparison banks’ rates as of April 23, 2024.

National Average rate effective as of April 23, 2024.

Compounding frequency. Compounding frequency is the time period at which the interest you earn is added to the balance. Not every bank or account compounds interest with the same frequency. Some may compound it monthly, while others compound daily.

Fees. The more you have to pay in fees, the less you can put towards your savings goals. So you’ll want to review the fee schedule carefully when you’re looking at a savings account. Some common ones you may come across are monthly maintenance fees, statement fees, and minimum balance fees.

FDIC insurance. Before opening an account, make sure that your bank is a member of the FDIC. It’ll give you peace of mind in knowing that your deposits will be insured up to the maximum allowable by law.

Popular types of savings accounts

At Marcus, when we talk about a savings account, we’re generally referring to our Online Savings Account. However, there are other types of deposit products that could help you save and earn interest. Knowing how these different products work can help you put together a savings plan that makes sense for your goals.

Here are a few types of savings products that banks and credit unions commonly offer.

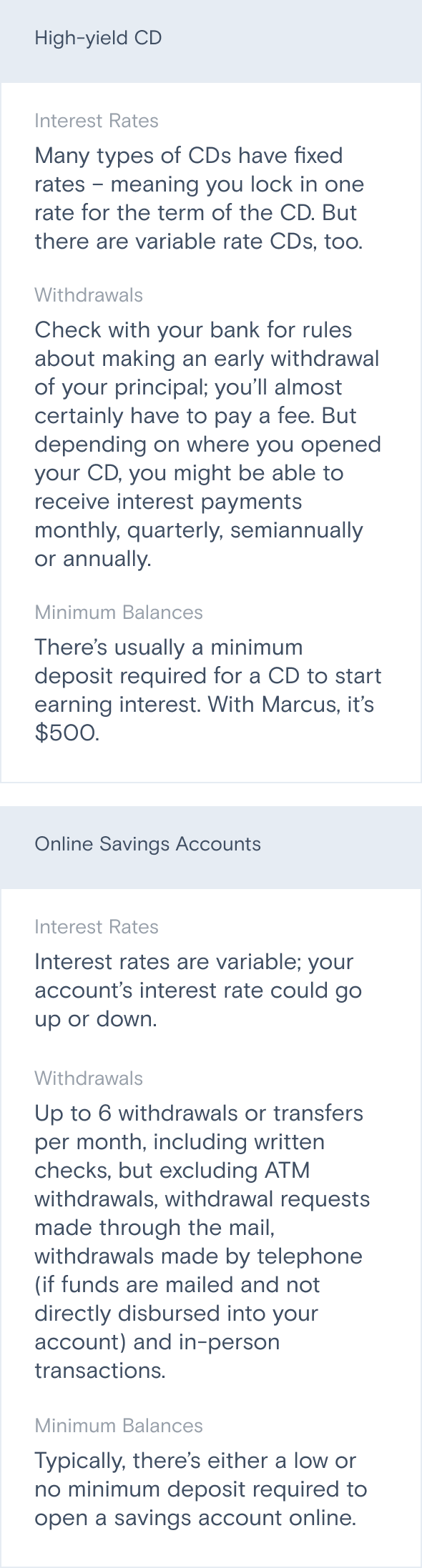

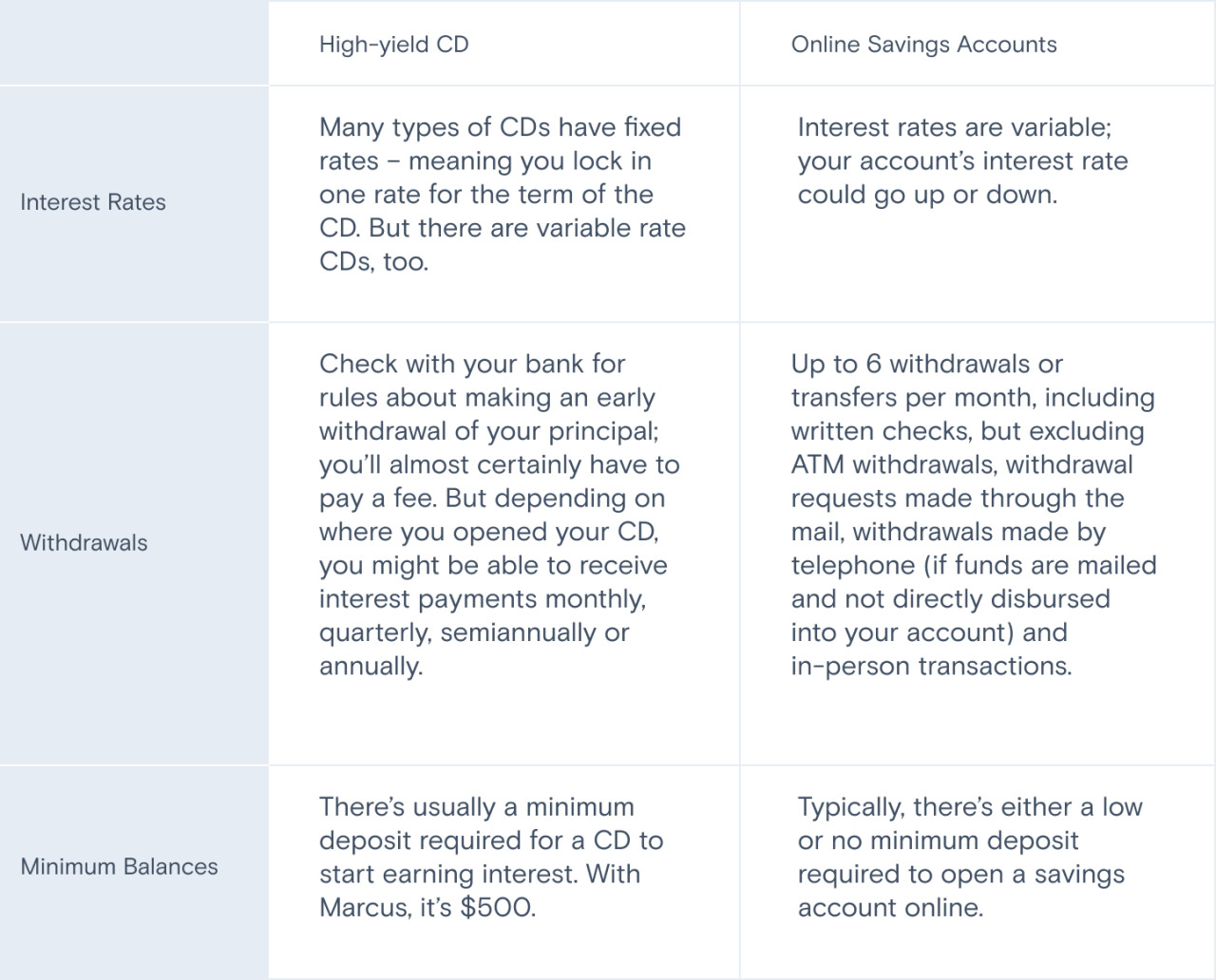

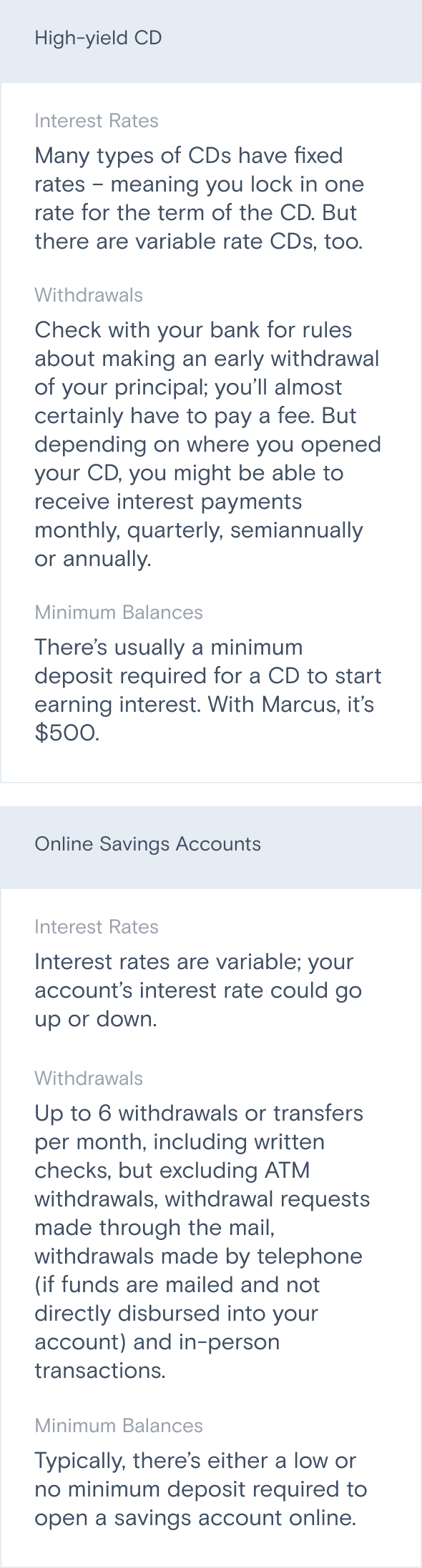

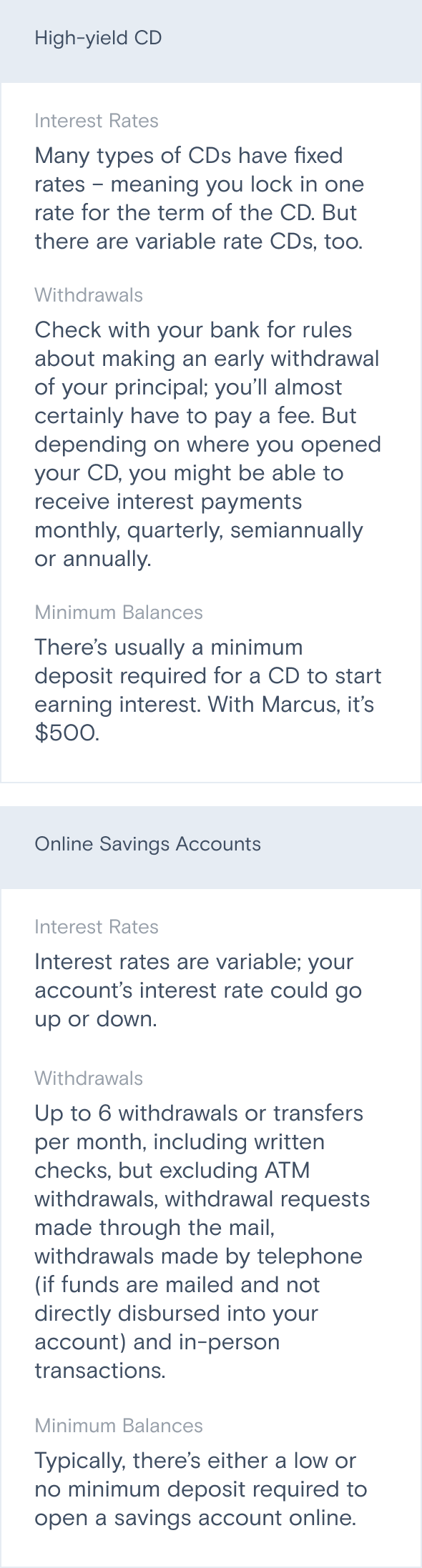

Traditional and high-yield savings accounts

You can find these accounts at brick-and-mortar banks, online banks, and credit unions. These accounts allow you to deposit money on a regular basis and withdraw funds relatively easily. High-yield savings accounts could offer higher APYs than traditional savings accounts.

- How it works: You can add money as often as you’d like and earn interest.

- Minimum balance: It depends on the bank, but the minimum requirement tends to be low.

- Withdrawals: Withdrawals may be limited to 6 per month, depending on your bank and the type of withdrawal you make.

- Interest rates: Savings accounts have variable rates, so they can go up or down.

- Things to look out for: APY, compounding frequency, fees

Certificates of deposit (CDs)

These accounts often come with a fixed rate and offer a higher APY than regular savings accounts. In exchange for the higher rate, you have to keep your money in the account for a predetermined period of time. If you take your money out before the CD matures, you’ll likely have to pay an early withdrawal penalty – unless it’s a no-penalty CD.

No-penalty CDs (NPCDs) offer a little more flexibility when it comes to withdrawals. You can withdraw your full balance before the end of the CD term without penalty (usually after a short initial waiting period after funding). But NPCDs typically offer lower APYs than traditional CDs.

- How it works: You can deposit money only during the initial funding period. With traditional CDs, you keep the money deposited until the maturity date. Taking money out before the maturity date can result in an early withdrawal penalty – unless you have a no-penalty CD.

- Minimum balance: The minimum amount will vary depending on the bank.

- Withdrawals: With a traditional CD, you can withdraw your funds when your CD matures. With a no-penalty CD, you may withdraw your money before the maturity date after an initial waiting period.

- Interest rates: Typically fixed, which means a guaranteed return if you keep all of the money, including interest, in the account for the full term.

- Things to look out for: APY, length of CD term, compounding frequency, fees, account minimums.

Read more: Guide to CDs

See how much interest you could earn with a Marcus high-yield CD.

Money market accounts

Money market accounts tend to offer lower APYs than CDs, but they offer flexibility when it comes to deposits and withdrawals. For instance, you can add money on a regular basis and may be able to withdraw funds with a debit card. Some accounts also offer check-writing privileges. However, banks may limit the number of transactions you can make each month.

- How it works: You can add money as often as you’d like and earn interest. Some accounts may include a debit card and check-writing privileges.

- Minimum balance: There’s usually a minimum requirement; the amount varies bank to bank.

- Withdrawals: You can usually make unlimited withdrawals, but some banks may impose a monthly limit.

- Interest rates: Money market accounts offer variable rates, so they can go up or down.

- Things to look out for: APY, compounding rate, fees, transaction limits.

Types of savings accounts

Savings Account (traditional or online)

Certificate of Deposit

No-Penalty CD

Money Market Account

|

Savings Account (traditional or online) |

Certificate of Deposit |

No-Penalty CD |

Money Market Account |

|

|---|---|---|---|---|

|

APY |

Variable rate |

Typically a fixed rate |

Typically a fixed rate |

Variable rate |

|

Minimum deposit requirements |

Typically, yes |

Yes |

Yes |

Typically, yes |

|

Withdrawals |

Withdrawals may be limited to 6 per month, depending on your bank and the type of withdrawal you make. |

You may pay a fee if you withdraw the principal before the CD term ends. |

You can withdraw your money after an initial waiting period (usually 7 days after funding) without having to pay a penalty. |

Withdrawals may be limited to 6 per month, depending on your bank and the type of withdrawal you make. |

|

Potential uses |

Saving money and earning interest, while keeping funds in easy reach. |

Saving money and earning interest for time-bound goals, like a down payment or vacation. |

Saving for a time-bound goal and earning interest without having to commit to a full CD term. |

Saving money and earning interest while maintaining liquidity via debit card or check-writing privileges. |

|

Where you can open them |

Banks and credit unions |

Banks and credit unions |

Banks and credit unions |

Banks and credit unions |

Open a savings account to support your goals

If you’re trying to decide which type of savings account to open, consider your needs and goals. What’s the timeline of your goals? Do you need flexibility when it comes to accessing your cash?

You may come to find that you want to use a combination of different savings vehicles. For instance, some people may have both a high-yield savings account and a CD – each designated for a different goal.

Let’s take a look at a few basic examples.

- Emergency fund. An emergency fund is money you set aside to help cover any unexpected expenses, such as a medical emergency or urgent home repairs. Many financial experts generally recommend having enough in your emergency fund to cover at least three to six months of living expenses. Accounts that could be useful here include an high-yield savings account or money market account if you want to add money as you go and easily make a withdrawal when you need the funds. You may also want to look into a no-penalty CD account where you could earn a competitive rate and have the flexibility to withdraw your funds. Just remember that with no-penalty CDs, once you open an account and make a deposit, you can’t continuously add money to it.

- A near-term goal like a dream vacation or home renovation. If you already have some money set aside in a traditional savings account for a short-term goal, you may want to consider putting that money into a high-yield CD instead, where you could earn a higher interest rate. Just make sure you don’t need the funds for something else right now, like an emergency fund. Remember, when you fund a CD, you’re committed to keeping your money deposited for a fixed period of time. Taking money out before a CD matures will result in an early withdrawal penalty (unless it’s a no-penalty CD).

- Locking in different CD rates. Here are some strategies you may want to consider:

- A CD ladder is a savings strategy where you spread your money across multiple CDs with different maturity dates. The goal is to lock in high APYs over time across multiple CDs. And as those CDs mature, you can either take out your money to spend or roll it over to a new CD to continue your ladder.

- A CD barbell involves splitting a pool of money and putting funds into short-term and long-term CDs. For example, you could open two CDs – one for short term and one for long term – and deposit half your money into each. The goal is to earn a higher average yield than you would have if you had simply put that money into a traditional savings account or short-term CDs. At the same time, the barbell strategy offers flexibility for you to access a portion of your savings once the short-term CDs mature.

Content to keep you on the path to financial well-being.

This article is for informational purposes only and is not a substitute for individualized professional advice. Articles on this website were commissioned and approved by Marcus by Goldman Sachs®, but may not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions.

Related Content

5 min read

5 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!