Why the Fed Cares About Your Inflation Worries

Share this article

On June 15, the Federal Reserve hiked the Fed funds rate by 0.75% – their biggest jump in nearly 30 years. The move came only a month after Fed Chair Jerome Powell assured us a rate hike that big wasn’t “something the Fed is actively considering.” What changed the Fed’s mind?

Actually, it was all of us–consumers, businesses and investors. Our inflation expectations were the thunderclap that pushed the Fed to speed up its storm preparations, raising rates to help cool the inflation we saw as a growing threat.

Here’s how and why our inflation expectations have so much influence with the Fed.

What are inflation expectations?

Inflation expectations are simply the pace of price increases we expect to see in the future. These expectations are influenced by several factors including:

- Our experience of past inflation. This is probably the key factor in our expectations. If inflation has been mild for a long time, we can have trouble believing it will get out of hand. But when we’ve had a little experience of inflation running high, we start believing that will continue. Something called “recency bias” leads us to believe the future will look much like the recent past, whether the evidence backs this up or not.

- Our frequent transactions. Gas and food make up only about 15% of the average American household budget. But since we run into these prices on a weekly or even daily basis, they can have an outsized effect on our inflation expectations.

- News stories, political ads and dinner table talk. The more we read, hear and talk about soaring inflation, the more we’re likely to believe that inflation is – and will continue to be – rising out of control. And our colleagues in Global Investment Research point out that inflation worries may get magnified during the run-up to this year’s midterm elections. Voters consider inflation one of the main issues this fall, and data suggests that inflation-related campaign ads could fuel inflation concerns and help shape consumer expectations.

Inflation can be a self-fulfilling prophecy

The Fed pays close attention to our expectations of inflation, because they know we tend to get the inflation we expect.

How does this work? Our expectations often affect our personal financial decisions that can in turn impact inflation. As workers, if we believe prices are rising quickly, we’re likely to ask for higher raises. When employers expect to have to grant substantial raises, they may increase prices to cover labor costs. (If left unchecked, these back-and-forth responses become an inflationary loop called the “wage-price spiral.”)

As consumers, if we’re expecting prices to rise, we’re more likely to accept these price increases and keep buying from these businesses. In fact, we may actually increase our short-term purchasing – buying items sooner to dodge future price hikes. This increases short-term demand which, if it outstrips supply, can fuel even higher inflation.

The Fed moves quickly on expectations news

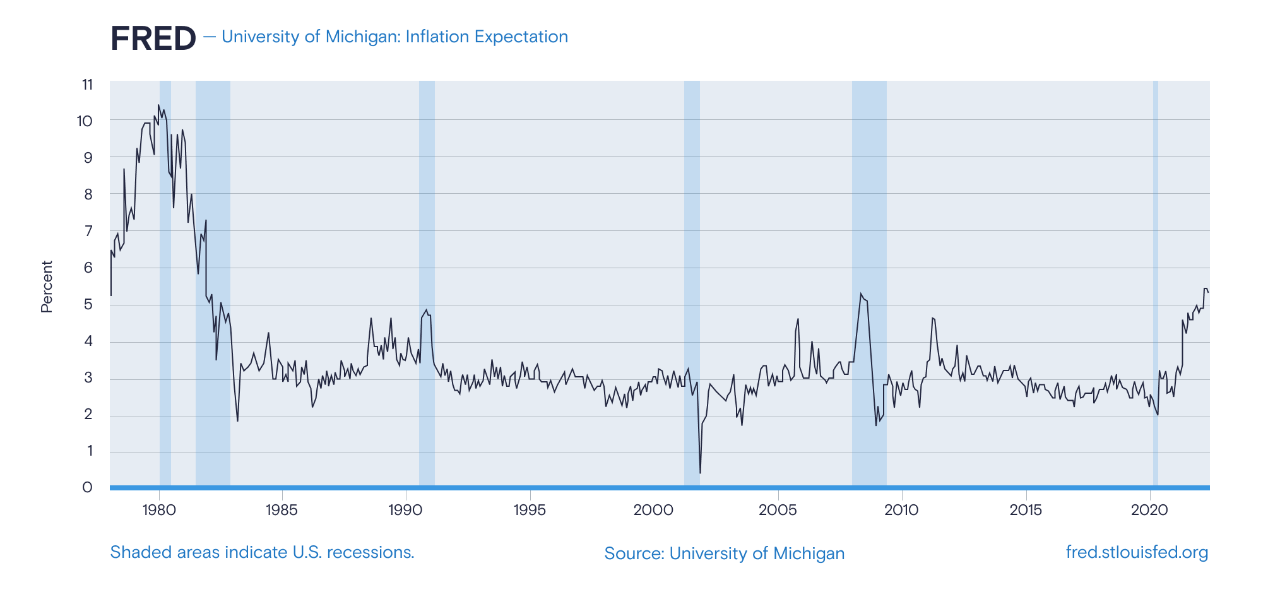

A recent bump in our inflation expectations caught the Fed’s attention. In June, days before the next Fed rates meeting, the University of Michigan’s Survey Research Center released its latest data showing that households expect long-term inflation to run at 3.3%, one of the highest levels since the mid-1990s (see chart below). Consumers also said they felt worse about their current financial situation than they had since 2013, and many blamed inflation.

The University of Michigan results came out June 10 (along with higher consumer price index data). The first reports that the Fed was considering a 0.75% rate hike were published on June 13. The hike took place on June 15.

The speed of this reaction is important. Communication is as important a tool of Fed policy as their rate hikes. Whenever the Fed alerts us to its likely future actions (a strategy known as “forward guidance”), that becomes part of the mass of swirling information that forms our expectations. Lately, they’ve been announcing what they plan to do a few months in advance to give consumers and the markets time to adjust to what’s coming. But when this news came out, they reacted quickly.

Anchoring against the storm

The Fed responded so quickly because the data showed them that they needed to do more to keep inflation at bay. For the past few months, members of the Fed have been trying to “anchor” inflation expectations through congressional appearances, media interviews and rate hikes, but these actions apparently had not been enough.

Anchoring basically means making sure consumers’ long-term inflation expectations are relatively stable and impervious to short-term shocks such as a temporary spike in gas prices. It’s securing our economic boat against squalls. The goal for long-term inflation expectations, from the Fed’s point of view, is to “anchor” them at roughly 2% well below the 3.3% revealed by the Michigan study. (2% is the level of inflation the Fed considers “ideal.”)

If consumers and businesses aren’t worried about runaway inflation and confident about the Fed’s ability to keep it stable, they’re less likely to make financial decisions that could drive inflation higher like asking for large raises, raising prices significantly or stocking up on purchases.

On the other hand, if consumers lose faith in the Fed or feel confused about its future actions, they could make decisions that contribute to higher inflation. The Fed is trying hard to avoid this.

The inflation outlook

While our expectations can certainly move the needle on prices, we know they’re not the only thing that impact inflation – major events like a pandemic, supply-chain disruptions, war in Europe and a tight labor market have all tipped us into this inflationary period. However, our Research colleagues believe inflation will likely start to moderate by year-end and continue dropping over the next two years.

That said, they also point out that the risks of wage growth, oil price spikes and political messaging remain with us. It’s important for the Fed to follow through with its storm preparations and quiet our self-fulfilling worries.

This article is for informational purposes only and is not a substitute for individualized professional advice. Individuals should consult their own tax advisor for matters specific to their own taxes and nothing communicated to you herein should be considered tax advice. This article was prepared by and approved by Marcus by Goldman Sachs, but does not reflect the institutional opinions of Goldman Sachs Bank USA, Goldman Sachs Group, Inc. or any of their affiliates, subsidiaries or division. Goldman Sachs Bank USA does not provide any financial, economic, legal, accounting, tax or other recommendation in this article. Information and opinions expressed in this article are as of the date of this material only and subject to change without notice. Information contained in this article does not constitute the provision of investment advice by Goldman Sachs Bank USA or any its affiliates. Neither Goldman Sachs Bank USA nor any of its affiliates makes any representations or warranties, express or implied, as to the accuracy or completeness of the statements or any information contained in this document and any liability therefore is expressly disclaimed.

1 min read

1 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!