When the Fed Tapers, What's Your Move?

Share this article

Marcus by Goldman Sachs is excited to share some insights about Fed tapering and how it could affect your portfolio from our friends at Goldman Sachs Asset Management.

Fed tapering. You’ve probably heard about it lately, with the Fed’s announcement that it will begin to gradually slow “or taper” the pace of its stimulus measures.

But even if you understand exactly what tapering is – and it’s no shame not to, the Fed is a meaty subject even for experts! – you may be wondering if and how it could affect your investing strategy.

According to our friends at Goldman Sachs Asset Management, “the best approach may be to stay invested and remember the important role that high quality intermediate duration fixed income plays within a well-balanced portfolio.”

But before we get into their thoughts on why, let’s go over what tapering is and how it relates to the economy.

One way the Fed balances the economy

Let’s start with a brief review of the mysterious ways of the Federal Reserve. (Feel free to skip ahead if this is old hat to you.) It’s easier to understand tapering if we first understand why and how the Fed influences interest rates.

Much of the Fed’s job is to keep the US economy stabilized, which according to the Fed’s mandate, means it’s operating “with stable prices and maximum employment.”

When we have those, the Fed can leave interest rates alone to do their own thing.

But when the economy is struggling, the Fed can buy Treasury bonds and other securities on the open market to push interest rates down. Lower interest rates stimulate borrowing, investment, job creation and economic activity.

The Fed can also sell these securities to drive interest rates up. Higher interest rates stimulate saving and cool the economy.

That sounds pretty straightforward! Now let’s dive in a little deeper.

The Fed will first focus on adjusting short-term rates. But sometimes it needs a different strategy, especially in times of crisis.

Let’s use Covid as an example: When the Covid pandemic hit and the economy started to shut down, the Fed was faced with a need to quickly stimulate the economy. Time to lower interest rates!

The problem, however, was that short-term interest rates were already near zero.

Our Federal Reserve (unlike some foreign central banks) prefers not to lower the fed funds rate below zero. So, when they start to run out of positive numbers, the Fed can turn to a process called Quantitative Easing (QE).

This strategy is similar to the Fed’s usual interest-influencing activities but targets longer-term interest rates.

In the beginning of Covid, the Fed committed to making huge purchases of long-term securities – 10-year Treasury bonds and mortgage-backed securities – adding $4 trillion of assets to its balance sheet from late 2019 to November 2021.

This move was intended to drive down longer-term rates and stimulate investment and confidence in the economy.

So, what is Fed tapering?

Let’s finally get to tapering. When the Fed tapers, it winds down its QE activities, buying fewer securities each month.

The Fed begins tapering when it feels more confident about the strength of the economy.

And that’s a good thing! But, even during the tapering process, the Fed will keep a close eye on the economy’s progress and adjust its path if necessary.

Should Fed tapering affect your bond strategy?

When a major buyer like the Fed slows down its buying, the supply of bonds that other investors can purchase rises. Because of this, bond prices tend to drop and interest rates rise.

You might remember the 2013 “taper tantrum” when an off-the-cuff announcement by the Fed’s chairman led to financial uneasiness.

But our friends at Goldman Sachs Asset Management believe the Fed’s careful messaging this time around and its reasonable policy path should stave off panic.

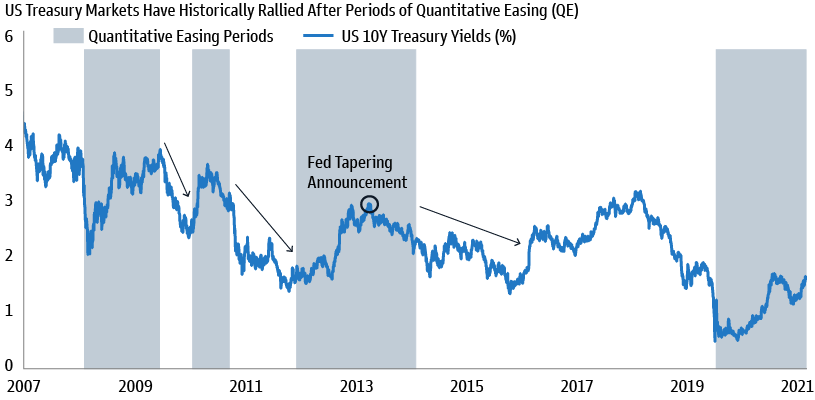

To see how things might shake out this tapering round, they suggest taking a look at past patterns in the bond market.

Naturally, we can’t depend on history to repeat itself, but it helps to understand it.

If you look at the chart below, you can see that the 2013 tapering announcement led to higher US 10-year Treasury yields and lower prices. (Interest rates are also called yields, when you’re talking about bonds and Treasuries.)

But, looking back, we also see that in 2013 and other tapering periods, initial rate spikes and price drops were followed by a swing in the opposite direction that produced nice returns for bond investors.

EXHIBIT 1: US TREASURY MARKETS HAVE HISTORICALLY RALLIED AFTER PERIODS OF QUANTITATIVE EASING (QE)

Source: Goldman Sachs Asset Management, Barclays Live. As of 10/25/2021. 10 Yr US Treasury yields proxied by the Bloomberg US 10 Yr Treasury Bellwethers Index.

For this round of tapering, our Goldman Sachs Asset Management friends believe pent-up demand from large institutional investors may keep prices and yields from swinging too wildly.

Whether or not this happens, some investors might stay the course and remember the important diversifying role of bonds and other high-quality fixed income in their portfolio.

And, if yields do rise, investors could consider using the extra income to buy while prices are low. A financial advisor can help you decide what makes sense for your individual portfolio.

This article is for informational purposes only and shall not constitute an offer, solicitation, or recommendation to buy or sell securities, or of an account type, securities transaction, or investment strategy. This article was prepared by and approved by Marcus by Goldman Sachs®, but is not a description of any of the products or services offered by and does not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions. Goldman Sachs Bank USA and Goldman Sachs & Co. LLC are not providing any financial, economic, legal, accounting, tax or other recommendation in this article and it is not a substitute for individualized professional advice. Information and opinions expressed in this article are as of the date of this material only and subject to change without notice. Information contained in this article does not constitute the provision of investment advice by Goldman Sachs Bank USA, Goldman Sachs & Co. LLC are or any of their affiliates, none of which are a fiduciary with respect to any person or plan by reason of providing the material or content herein. Neither Goldman Sachs Bank USA, Goldman Sachs & Co. LLC nor any of their affiliates makes any representations or warranties, express or implied, as to the accuracy or completeness of the statements or any information contained in this document and any liability therefore is expressly disclaimed.

Investing involves risk, including the potential loss of money invested. Past performance does not guarantee future results. Neither asset diversification or investment in a continuous or periodic investment plan guarantees a profit or protects against a loss.

Investment products are: NOT FDIC INSURED ∙ NOT A DEPOSIT OR OTHER OBLIGATION OF, OR GUARANTEED BY, GOLDMAN SACHS BANK USA ∙ SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED

3 min watch

3 min watch

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!