The Supply Chain Is Back!

Share this article

The state of the supply chain affects both how quickly we can get the goods we need and what those goods ultimately cost. Improvements are good both for the transportation business and consumers.

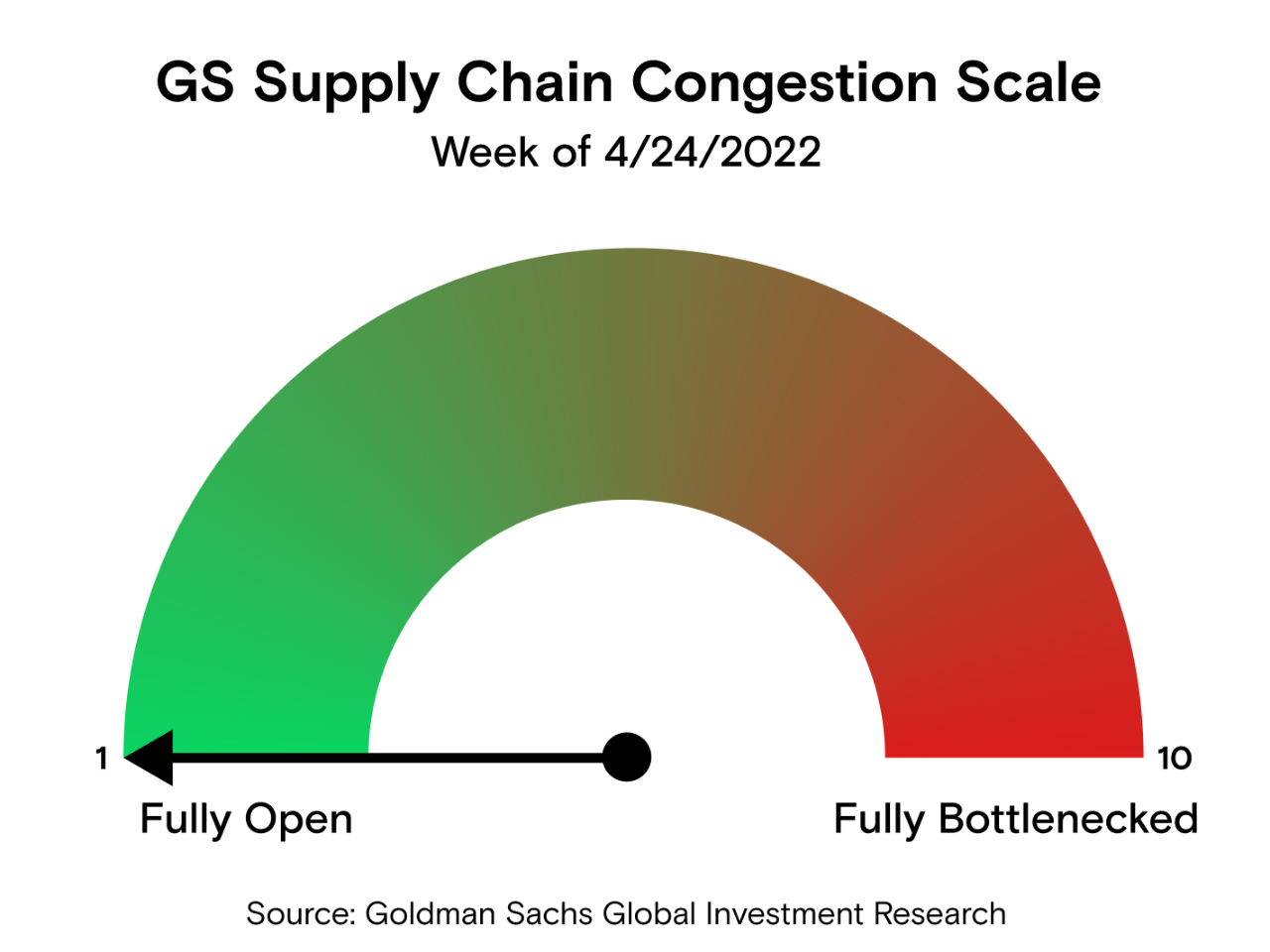

Given its importance to retailers, consumer goods companies and inflationary pricing, our colleagues in Goldman Sachs Research developed a proprietary scale to measure its health.

They put together data on ships backlogged off the east and west coasts, days to delivery, shipping container and chassis street dwell times, intermodal volume and more. The goal is to try to quantify the health of supply chains between being “Fully Bottlenecked” and “Fully Open” relative to before the pandemic (February 2020).

The good news? In late April, this scale fell to a level of 1 or Fully Open, marking an official return to the pre-pandemic supply chain environment, following three years of atypical congestion.

Let’s dive into some of the details:

- The number of container ships waiting to dock and unload goods along the West Coast remained at zero for the 21st consecutive week while there was a backlog of 4 ships on the East Coast during the week of April 24; the effective ship backlog remains near zero, which compares to over 100 ships backlogged during peak congestion.

- Shipping containers and railcars are spending less time waiting at port terminals.

- Rails and trucks are moving too. In intermodal traffic – moving freight by two or more modes of transportation – growth is improving.

Why are we seeing improvements?

- Transportation labor and equipment shortages have improved.

- Warehouse capacity and utilization have expanded.

- Consumer demand is moderating, taking some of the high-volume pressure off the system.

The key question remains whether the last stumbling blocks around congestion will soon ease – notably the still-full warehouses, as well as East Coast port backlogs. If so, it’s possible we could stay at level 1 throughout the first half of the year, at least.

This article is for informational purposes only and is not a substitute for individualized professional advice. Articles on this website were commissioned and approved by Marcus by Goldman Sachs®, but may not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions.

Related Content

5 min read

5 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!