The Inflation Plot Thickens: What It Could Mean For Your Portfolio

Share this article

Marcus is excited to share some insights about how inflation might affect your investments from our friends at Goldman Sachs Asset Management.

Inflation has been a hot topic for months and it’s still with us. Hopefully, the past articles have helped you understand what inflation is and what it could mean for the economy. (Feel free to take time out here for a refresher, if it’s helpful.)

However, you may still have questions about what it could mean for your portfolio. Do rising prices lift all boats, including stock and bond prices? Does inflation lower the value of securities? Is it a mixed bag? Or business as usual?

We’ll start with a caveat: There’s a lot of uncertainty around factors that could affect inflation in the upcoming months, such as supply chain issues, Fed moves and the omicron variant, so predicting the price of a haircut next spring is tricky right now even for the experts.

However, we may be able to shed some light on how different inflation scenarios could affect your investments, with the help of our friends at Goldman Sachs Asset Management. They analyzed data from inflationary periods over the past 74 years to help give us an idea of what could happen to markets – and portfolios – as we head into 2022.

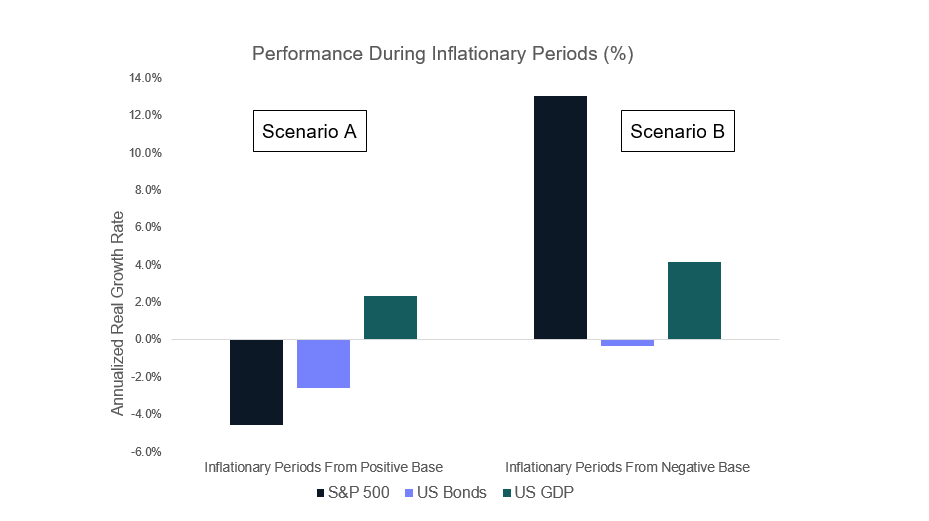

Tale of two inflation scenarios

Before the new season of a hit show starts, it can help to binge-watch past episodes and get some background. We’ve had 11 periods of rising inflation since World War II, giving us plenty of data to look back on. Now, every inflation event is a little different, which means the past won’t predict the future, but it can be interesting to look at patterns that have repeated.

Our Asset Management colleagues separated these 11 inflationary periods into two scenarios, based on what was happening to prices right before their rapid rise:

- Scenario A: a modest pace of price increases sped up – turning into high inflation.

- Scenario B: prices turned sharply around after a period of heading down (also known as deflation).

The big takeaway? These two scenarios historically affected stock and bond performance in very different ways. Let’s see how.

We can look at the real returns of the S&P 500 stock index and US bonds during these periods of rising inflation. (Real returns simply mean the total profits earned on an investment, adjusted for inflation.)

Performance During Inflationary Periods (%)

S&P 500

US Bonds

US GDP

|

S&P 500 |

US Bonds |

US GDP |

|

|---|---|---|---|

|

Inflationary Periods From Positive Base |

-4.6% |

-2.6% |

2.3% |

|

Inflationary Periods From Negative Base |

13.0% |

-0.4% |

4.2% |

Source: As of October 26, 2021. Federal Reserve Bank of St. Louis, Shiller, and Goldman Sachs Asset Management. The time period is from December 1947 to March 2021. US Bond Returns are derived from Shiller's database and implied by the monthly market yield on U.S. treasury securities at 10-year constant maturity. Arithmetic average of the performance of the periods identified. Past performance does not guarantee future results, which may vary.

As you can see in the chart, when there was rising inflation after a period of modest but positive inflation (Scenario A), both stocks and bonds were down during these periods.

Stock performance may have gone down because higher costs for raw materials and services can decrease corporate profit margins. And poorer bond performance could be a reaction to investors’ concerns that the Federal Reserve will raise interest rates to cool inflation. Remember, higher interest rates generally mean lower bond prices.

In Scenario B, when rising inflation followed after negative inflation (deflation), however, stocks were up and bonds were only slightly negative during that period.

In this scenario, rising inflation is – at least at first – a welcome arrival. Corporate profit margins may increase if companies can get more for the goods and services they sell. At the same time, to make up for years of deflation, the Fed may consider letting inflation run up a little higher than their usual 2% target. The less they move to raise interest rates, the less bond prices tend to drop.

What inflation could mean for your portfolio in 2022

Whew. Thanks for sticking with us this long. Bottom line – which scenario are we in now? Inflation was relatively low (below the Fed’s 2% target) during the decade prior to the pandemic, and it fell even lower during the pandemic, but stayed mildly positive. This suggests a gentle Scenario A, but there are one or two more things to look out for inflation-wise in 2022.

You’ve probably heard the pundits hotly debating whether this bout of inflation is transitory or persistent; in other words, how long can we expect prices to keep going up? Our Asset Management folks suggest that the duration of inflation matters for the markets. A long-lasting rise in prices can negatively affect both stocks and bonds, while a temporary spike (less than 2 years) may be less damaging.

If the inflationary spike we’re in now is temporary, we should see disinflation – a slowdown in inflation – at some point in 2022, and our friends at Asset Management think this is likely. What would this mean for your investments? The short answer (and the good news): Stocks and bonds both have the potential to do well in most disinflationary periods.

Omicron, supply chain issues, the Fed’s decisions… As we mentioned earlier, there are a lot of unsettled factors on the horizon that could ultimately affect inflation and the markets in the upcoming year. And remember that historical performance doesn’t predict future results.

Goldman Sachs Asset Management still favors equities for 2022, but uncertainty can feel uncomfortable for investors. Read our pointers for how to invest in uncertain times, plus don’t forget you don’t have to go it alone. Talk to your financial advisor for recommendations on how to handle your individual portfolio.

This article is for informational purposes only and shall not constitute an offer, solicitation, or recommendation to buy or sell securities, or of an account type, securities transaction, or investment strategy. This article was prepared by and approved by Marcus by Goldman Sachs®, but is not a description of any of the products or services offered by and does not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions. Goldman Sachs Bank USA and Goldman Sachs & Co. LLC are not providing any financial, economic, legal, accounting, tax or other recommendation in this article and it is not a substitute for individualized professional advice. Information and opinions expressed in this article are as of the date of this material only and subject to change without notice. Information contained in this article does not constitute the provision of investment advice by Goldman Sachs Bank USA, Goldman Sachs & Co. LLC are or any of their affiliates, none of which are a fiduciary with respect to any person or plan by reason of providing the material or content herein. Neither Goldman Sachs Bank USA, Goldman Sachs & Co. LLC nor any of their affiliates makes any representations or warranties, express or implied, as to the accuracy or completeness of the statements or any information contained in this document and any liability therefore is expressly disclaimed.

Investing involves risk, including the potential loss of money invested. Past performance does not guarantee future results. Neither asset diversification or investment in a continuous or periodic investment plan guarantees a profit or protects against a loss.

Investment products are: NOT FDIC INSURED ∙ NOT A DEPOSIT OR OTHER OBLIGATION OF, OR GUARANTEED BY, GOLDMAN SACHS BANK USA ∙ SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED

Related Content

3 min read

3 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!