How GS Economists Think About 3 Major Recession Risks

Share this article

It’s THE question of the moment - is the United States on the brink of a recession? Everyone has an answer. The consensus forecast puts our chances of being in a recession within the next 12 months at 63%. Some economists believe the risk is as high as 100%.

Our colleagues at Goldman Sachs Global Investment Research, however, see things a little differently. They don’t believe the US economy is about to enter a recession right now. And their recession odds of 35% over the next year haven’t changed dramatically in past months.

This forecast is well below the consensus odds. Why do our colleagues take this view? They recently dove into three potential recession risks. Here’s a peek into their analysis.

1. The risk that a recession will be necessary to bring inflation down

The odds that a recession will be necessary to win the battle with inflation have actually fallen a little, according to our colleagues.

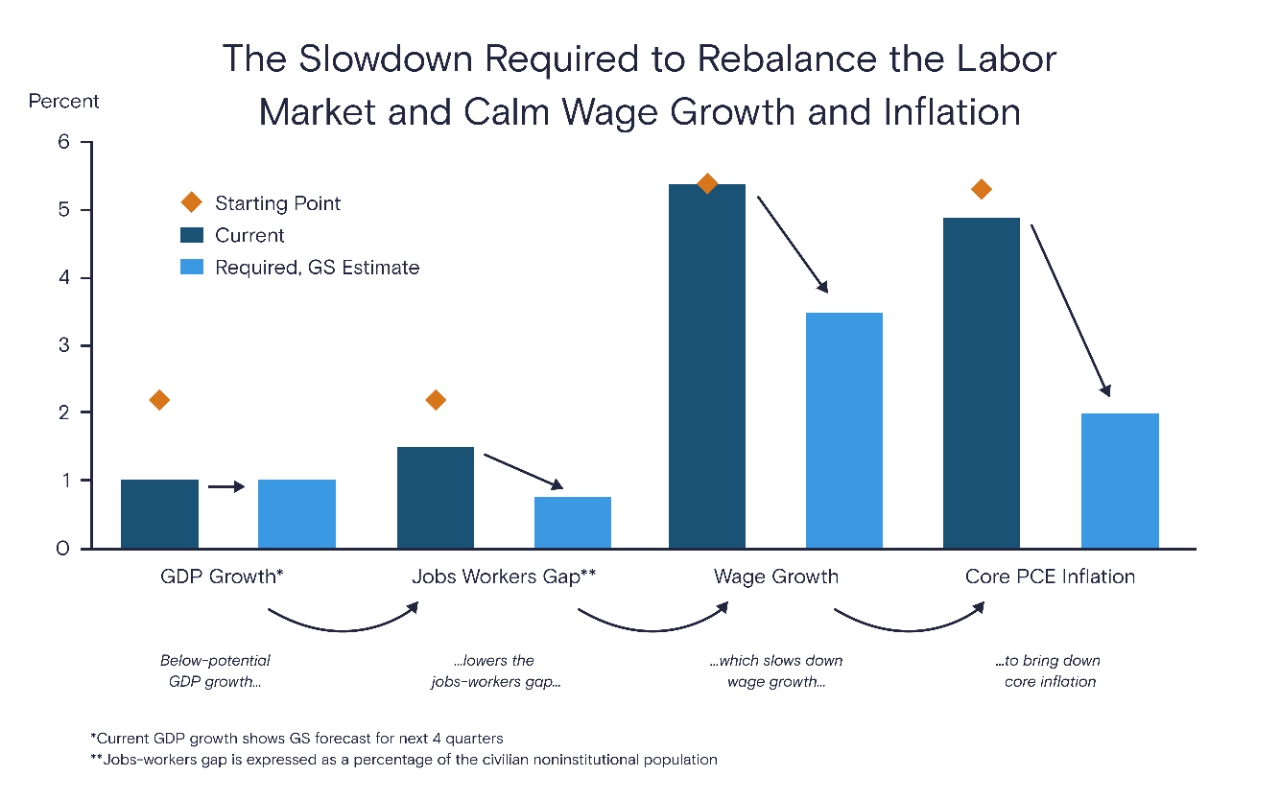

That’s because the first two steps to bring down inflation have gone remarkably well so far.

- We’ve started to slow GDP (gross domestic product) growth, which can help curb demand and give lagging supply a chance to catch up.

- We’ve made progress on reducing the oversized gap between jobs and workers in the US, which is fueling wage growth. In fact, that gap has already shrunk by nearly 50% of the amount our colleagues believe is necessary to reach a desired level of wage growth by the end of 2023.

But it’s still early. Our colleagues are waiting to see consistent evidence that labor market rebalancing is slowing wage inflation and breaking the wage-price loop.

Here’s a handy chart that our economists put together to illustrate how these factors relate to each other. The chart shows the progress we’ve made toward calming inflation and how far our colleagues believe we still need to go.

2. The risk that the Fed will cause a recession that is not necessary

This risk might have gotten a little higher recently. It’s becoming clear that shelter and health care inflation will probably stay uncomfortably high throughout 2023, even if the labor market rebalances effectively.

Since shelter and health care have a big impact on commonly used measures of inflation, our colleagues see some risk that the Fed could focus too much on these lagging indicators, grow impatient with stubborn overall inflation numbers or tighten too quickly to see the full impact of their actions on the economy. Unfortunately, any of these responses have the potential to push us into a recession.

3. The risk that some unforeseen factor will cause a recession

With so much uncertainty around the globe, this risk is likely somewhat higher than usual. Our Research colleagues doubt the slowdown in global GDP is enough to tip the US into a recession, but it’s hard to predict the impact of potential disturbances from international markets.

TL;DR: Goldman Sachs economists still see only a 35% probability of a recession over the next year, and think any recession would likely be mild. They are particularly skeptical of the common view that Fed rate hikes of the size expected, or even a little larger, will be enough to cause a recession.

This article is for informational purposes only and is not a substitute for individualized professional advice. Individuals should consult their own tax advisor for matters specific to their own taxes and nothing communicated to you herein should be considered tax advice. This article was prepared by and approved by Marcus by Goldman Sachs, but does not reflect the institutional opinions of Goldman Sachs Bank USA, Goldman Sachs Group, Inc. or any of their affiliates, subsidiaries or division. Goldman Sachs Bank USA does not provide any financial, economic, legal, accounting, tax or other recommendation in this article. Information and opinions expressed in this article are as of the date of this material only and subject to change without notice. Information contained in this article does not constitute the provision of investment advice by Goldman Sachs Bank USA or any its affiliates. Neither Goldman Sachs Bank USA nor any of its affiliates makes any representations or warranties, express or implied, as to the accuracy or completeness of the statements or any information contained in this document and any liability therefore is expressly disclaimed.

Related Content

2 min read

2 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!