xx

Marcus Invest Portfolio Changes: Putting Our Expertise to Work for You

June 28, 2021

Share this article

What we'll cover:

- From time to time, Marcus Invest makes strategic asset allocation changes, so that our customers may benefit from Goldman Sachs’ latest investment research and analysis

- Portfolio adjustments will be made for you over time as needed

- At Marcus Invest, we’re constantly looking for ways to optimize our portfolios to help maximize returns over time while balancing risk

Automating your investing with Marcus Invest means that you can spend your time elsewhere doing the things you love. That’s because our team, with the help of proprietary technology, takes care of many investment activities for you – from portfolio construction to daily monitoring and periodic rebalancing.

While automation can be a huge time-saver, we don’t leave everything up to algorithms.

When it comes to managing your portfolio and asset allocation strategy, we have a team of dedicated investment professionals (yes, humans – and really smart ones!) hard at work behind the scenes.

Portfolio research. Quantitative modeling. Market and economic trends analysis. You can leave all this fun homework to our experts in the Investment Strategy Group (ISG). An important part of their job is designing the asset allocation models for our portfolios at Marcus Invest to help maximize returns over time while managing risk.

In addition to helping us out at Marcus Invest, ISG also provides asset allocation advice to clients and businesses across Goldman Sachs, including Private Wealth Management and Personal Financial Management.

And based on ISG’s work, Marcus Invest is making an important change to our strategic model portfolios. Specifically, we’re adjusting the weight of investments in US public equities (read: stocks).

While you may not necessarily notice the effects of this change right away in your Marcus Invest portfolio, we want to keep you informed. We’re also excited to show you the work we’ve put in when it comes to managing your investments.

Remind me, what are strategic model portfolios? When Marcus Invest puts together a portfolio(s) for our customers, we don’t build them completely from scratch each time. We rely on a set of pre-built portfolios or model portfolios* . Generally, each model portfolio has its own specific strategic asset allocations and diversified group of assets that correspond to a certain level of risk and expected return.

*Marcus Invest offers portfolios based on models designed by GS&Co’s Investment Strategy Group (“ISG”), that allocate assets among ETFs representing different asset classes (each, a “Portfolio”).

What’s changing in Marcus Invest’s strategic model portfolios?

As we mentioned earlier, we’re adjusting the weight of investments in US public equities. Specifically, we’re increasing the US overweight within the strategic stock allocation.

If you’re still somewhat new to investing, you’re probably wondering what this means. Don’t worry – we’ll break it down for you and hopefully make this a not-so-intimidating read.

Let’s take, for example, a portfolio with the following target allocations: 60% stock ETFs, 40% bond ETFs (this part sounds familiar, right?).

When we say we’re “increasing the US overweight” in the strategic stock allocation, basically, it means that we want to change how we divvy up the stock investments. (We’re leaving the bond allocation side alone.)

If you look closely into the stock allocation of your portfolio, you can see that your money is typically invested across many different stock ETFs in a number of different regions. Some general categories may include US stocks, non-US developed stocks (Non-US) and emerging market (EM) stocks. Money may be invested equally between these categories. Or a greater portion may be allocated to one particular category.

In other words, different “weights” can be assigned to each asset category. For instance, in the Core 60 stock ETFs/40 bond ETFs portfolio, you might see the stock allocation split in the following way: 30% to US large cap equity, 17% to non-US equity, 3.5% to EM equity and 9.5% to other allocations.

Still with us? Great – now that you understand the concept of weights, let’s continue.

Since 2009, ISG has strategically allocated a greater portion of their equity portfolios to US stocks based on market research and analysis.1 Put another way, ISG has consistently recommended to overweight US stocks within the model portfolios.

When you see the term “US overweight,” what we’re essentially saying is that we’re favoring US stocks in our strategic asset allocations. Generally speaking, investors may choose to overweight an investment if they’re optimistic about the performance of a particular sector. In this case, our investment team is optimistic about the outlook for US public companies. (We’ll get into the reasons later.)

Now that we’ve given you some context, let’s revisit the question: What’s changing in our strategic portfolios?

Based on ISG research, we’re going to increase the US overweight within the stock allocation of our portfolios. The size of the allocation increase will vary, depending, in part, on the specific model portfolio we’re looking at. For example, in the Core 60/40 portfolio, the US large cap equity weight will increase from 30% to 32%.

Time is money. See how automating your investments could help.

What does this change mean for Marcus Invest customers?

Simply that, as Marcus Invest continues to manage and periodically rebalance your account, we’ll make sure your allocation stays aligned with both your goals and our updated recommendations. There’s no action you need to take, but we wanted to let you know that you may see a slight increase in the percentage of US stocks in your portfolio. (That is, if you have a stock allocation in your portfolio.) This change won’t affect all customers and will vary according to your individual account profile.

- Portfolio adjustments will be made for you over time as needed. You don’t have to lift a finger to adjust the weights of your stock investments. Marcus Invest will take care of that for you at the appropriate time. For example, we may make the adjustment when we’re rebalancing your portfolio or processing a deposit or withdrawal. Adjusting the US overweight in our model portfolios is a fine-tuning move, so you may not even notice any changes to your portfolio right away, if at all. And that’s the big idea behind automating your investing, right? We handle these technical changes behind the scenes, so you can focus on the big picture, like your investment goals.

- Helping you maximize returns over the long term while managing risk. Whenever Marcus Invest makes changes to our strategic portfolios, it’s because our investment team believes that certain adjustments might benefit our customers in the long run. Financial markets are complex and constantly in flux. And it’s our job to stay on top of economic and market trends for our customers, so that we can put our expertise to work for you, helping to identify growth opportunities while balancing risk.

- Bringing you expert investment research and analysis. Marcus Invest is powered by the expertise, insights and resources of Goldman Sachs. This change we’re making to our strategic model portfolios is based on the proprietary economic and market research conducted by ISG. And we’re bringing their investment expertise to you because as always, we are committed to helping you invest with more confidence.

The bottom line: As a Marcus Invest customer, your investments are in good hands. From time to time, we make changes to our strategic portfolios based on the proprietary economic and market views of our global economists and strategists. Our incredibly smart, savvy team of investment professionals work hard to stay on top of the latest trends to keep your money invested appropriately based on your risk tolerance and investment timeline.

If you’re interested in learning about the specific reasons why we’re increasing the US overweight in public equities, read on!

Information in the following sections is based on ISG’s economic and market analysis in the 2021 Outlook Report.

Why is Marcus Invest adjusting the US overweight in our stock allocation?

If you have time and want all the details, you might want to check out ISG’s 2021 Outlook Report. But while the report is super informative – showing the amount of work we put into formulating our investment and asset allocation strategies – we know that it’s not a breezy afternoon read.

So here’s the short answer: We’re increasing the US overweight in public equities in our strategic model portfolios because ISG believes that the US economy will maintain its leadership position globally and that US equities will continue to outperform non-US equities.2

ISG’s views on US preeminence in the global economy and financial markets aren’t a new development. In fact, the themes of US preeminence and staying invested have influenced ISG’s strategic asset allocation strategy for nearly a decade. Since 2009, ISG has consistently suggested that clients strategically allocate a greater portion of their equity portfolios to US stocks.3 And broadly speaking, over the years, US equities have outperformed both non-US developed equities and emerging market equities.4

“Our recommendation of US preeminence and staying invested has served our clients well,” Sharmin Mossavar-Rahmani, Goldman Sachs’ Chief Investment Officer for ISG, said during the Feb. 9, 2021, episode of Exchanges at Goldman Sachs. “People might think that those two themes have outlived their value, and our message is, no, continue with that theme.”

You may be wondering why ISG has such an optimistic outlook for the US economy and public companies. Does ISG have a crystal ball? Nope, ISG simply does their homework. Their confidence is based on three observations:

- US companies generate higher earnings growth compared to their counterparts around the world.5

- The US has more exposure to fast-growing sectors and remains at the forefront of innovation and technological advancement.6

- The US has more favorable demographics when it comes to the population of working-age adults.7

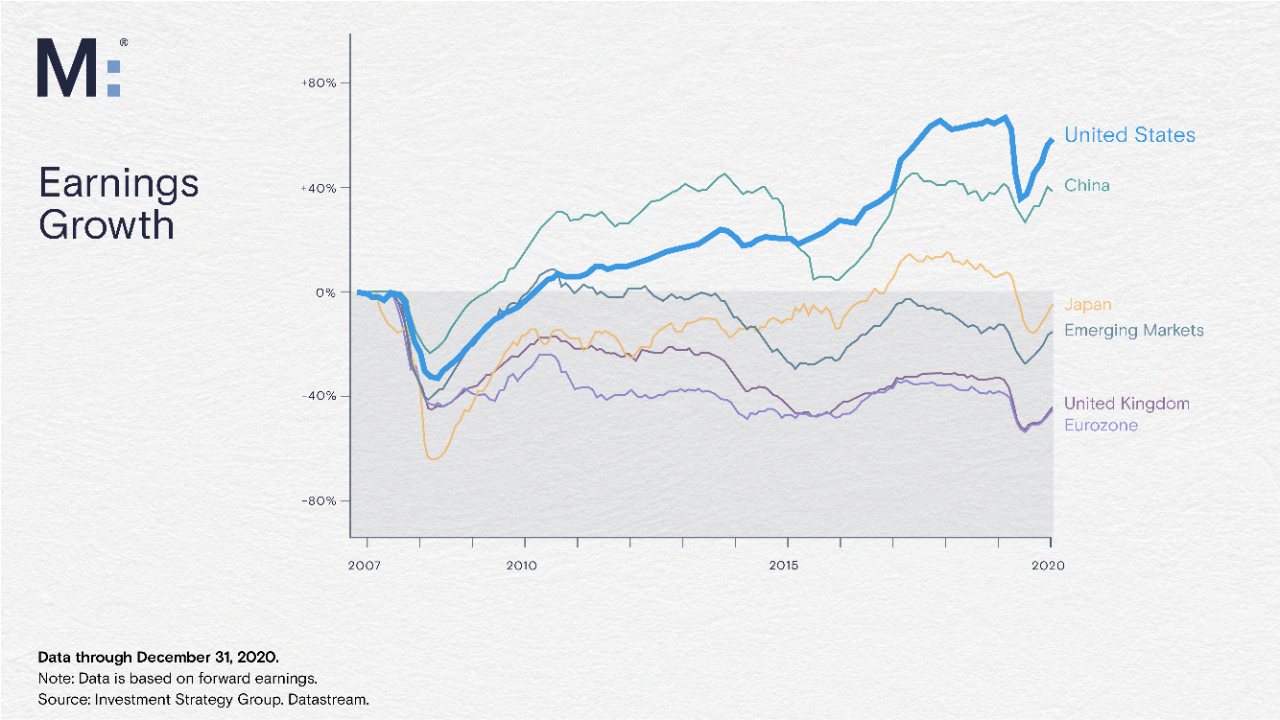

1. US companies generate higher earnings growth compared to their counterparts around the world

The strong earnings performance of US companies is a key reason why ISG continues to favor US public equities in our strategic portfolios.

If you take a look at the earnings growth chart below, you’ll see that US companies have generated much higher earnings growth (per share) than companies in other larger developed economies (relative to pre-global financial crisis levels).8

Another thing ISG has noted: Earnings outside the US have substantially lagged those of the US across most sectors since the peak in earnings growth in 2007.9

Why is that?

Many factors can account for the differences in earnings growth between US and non-US companies, including differences in corporate management, cost competitiveness and innovation.10

But broadly speaking, the US economy has certain structural advantages that could give US companies a leg up, which leads to our second point.

2. The US equity market has more exposure to fast-growing sectors compared with international equities

One potential reason for the relatively higher earnings growth is the higher exposure of US companies to fast-growing business sectors.

Compared with international equities, the S&P 500 is overweight in the following sectors: information technology, communication services and to a lesser degree, health care.11

That being said, even if we ignore the differences in sector exposure, US companies on the whole earn more than their non-US counterparts across other sectors as well.12

In other words, US outperformance isn’t limited to just one sector – the US outperforms non-US companies in other areas, too. This, again, bolsters our confidence in the US equities market.

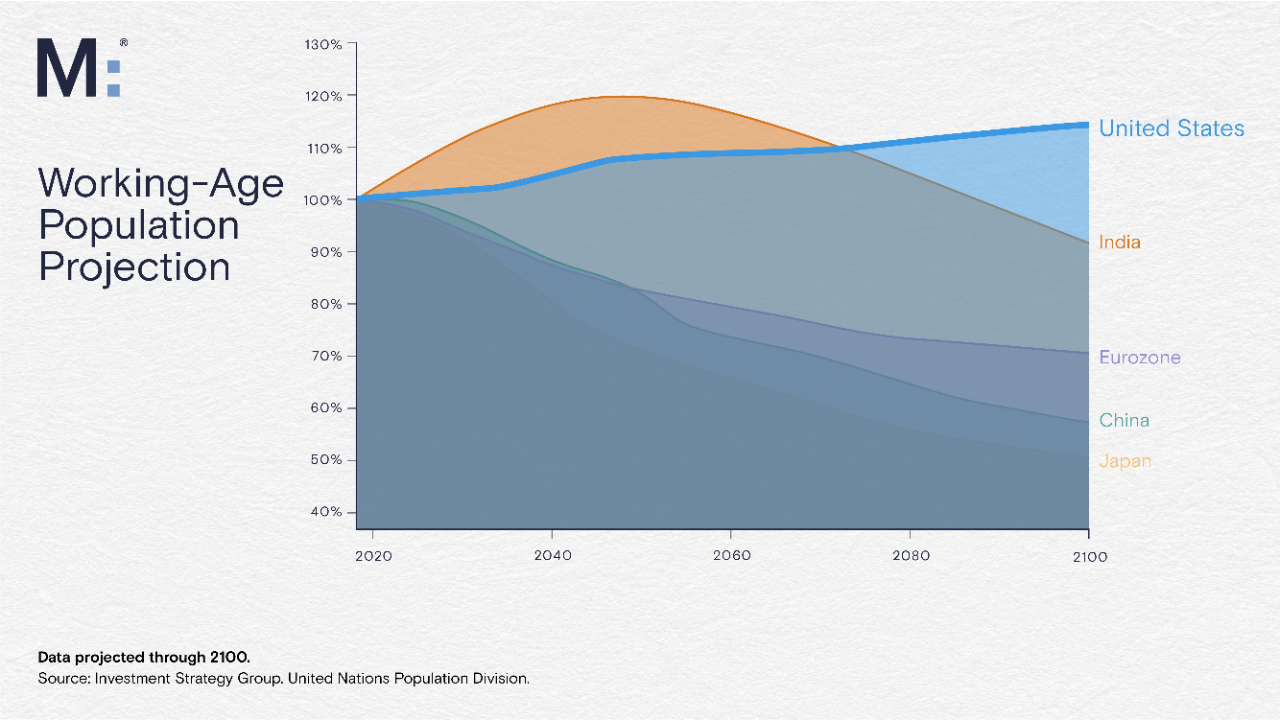

3. US has more favorable demographics than most other developed and emerging market countries

Another key advantage that the US has over other large, developed economies lies in its people.

Compared to many other economies, US demographics have a more favorable outlook – favorable in the sense that the working-age population of the US is not expected to peak in this century.13 More working-age people means more goods are produced and consumed, which helps drive economic growth.

Take a look at the projections for the US versus other large economies.

As you can see, the only country that has more favorable demographics over the next several decades is India.14

Now why do demographics matter? ISG takes demographics into consideration because a country’s population structure is a key indicator of economic growth.15

We won’t pull you into a full economics lecture here, but generally speaking, the larger the working-age population, the higher the economic output.

And this makes sense: The more people you have working, the more goods and services can be produced for the economy. A larger workforce also generally means higher consumer demand, consumption and investments, which are also drivers of economic growth.

On the other hand, countries with a low or shrinking working-age population (for instance, one with a low birth rate combined with an aging population) tend to see slower growth. These countries also have to allocate more resources to taking care of this aging population (think: income security and health care).

In short, favorable demographics in the US helps explain ISG’s confident outlook for US companies and the economy as a whole.

A recap

Thanks for sticking with us and letting us walk you through why Marcus Invest is increasing the US overweight in public equities in our strategic model portfolios. We know that was probably a lot of information to take in, but you made it!

From time to time, Marcus Invest makes strategic asset allocation changes, so that our customers may benefit from Goldman Sachs’ latest investment research and analysis. At Marcus Invest, we’re constantly looking for ways to optimize our portfolios to help maximize returns over time while balancing risk.

As a Marcus Invest customer, there’s no action you need to take due to this strategic update in our portfolios. We simply want to keep you informed of the work our investment professionals are doing behind the scenes and give you a heads up that you may see a slight increase in the percentage of US stocks in your portfolio’s stock allocation. Keep in mind that this change won’t affect all customers and will vary according to your individual account profile.

1. Investment Strategy Group. “Outlook 2021: US Resilient.” Goldman Sachs Private Wealth Management, January 2021, p. 1.

2. Ibid, p. 1-5.

3. Ibid, p.1.

4. Ibid, p. 26.

5. Ibid, p. 21-23.

6. Ibid, p. 37.

7. Ibid, p. 19.

8. Ibid, p. 22.

9. Ibid, p. 37.

10. Ibid, p. 21-26.

11. Ibid, p. 37-43.

12. Ibid, p. 37.

13. Ibid, p. 19.

14. Ibid.

15. Ibid.

This article is for informational purposes only and shall not constitute an offer, solicitation, or recommendation to buy or sell securities, or of an account type, securities transaction, or investment strategy. This article was prepared by and approved by Marcus by Goldman Sachs®, but does not reflect the institutional opinions of The Goldman Sachs Group, Inc., Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, subsidiaries or divisions. Goldman Sachs Bank USA and Goldman Sachs & Co. LLC are not providing any financial, economic, legal, accounting, tax or other recommendation in this article and it is not a substitute for individualized professional advice. Information and opinions expressed in this article are as of the date of this material only and subject to change without notice. Information contained in this article does not constitute the provision of investment advice by Goldman Sachs Bank USA, Goldman Sachs & Co. LLC or any of their affiliates, none of which are a fiduciary with respect to any person or plan by reason of providing the material or content herein. Neither Goldman Sachs Bank USA, Goldman Sachs & Co. LLC nor any of their affiliates makes any representations or warranties, express or implied, as to the accuracy or completeness of the statements or any information contained in this document and any liability therefore is expressly disclaimed.

Investing involves risk, including the potential loss of money invested. Past performance does not guarantee future results. Neither asset diversification or investment in a continuous or periodic investment plan guarantees a profit or protects against a loss.

Investment products are: NOT FDIC INSURED ∙ NOT A DEPOSIT OR OTHER OBLIGATION OF, OR GUARANTEED BY, GOLDMAN SACHS BANK USA ∙ SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED

Related Content

6 min read

6 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!