What Is a High-Yield Savings Account?

Share this article

Saving accounts seem pretty simple – add money to your bank account, earn interest, add more money, and make withdrawals as needed.

The money you tuck away can help you check off financial goals, whether that’s building up a nice emergency fund or having enough for a down payment.

But if you’re dropping money into a traditional savings account instead of a high-yield savings account, you could be shortchanging yourself. Both types of deposit accounts are a good place to park your funds.

But with a high-yield savings account (which is sometimes referred to as a high-interest savings account) your interest earnings could be higher.

Thinking about adding a high-interest savings account to your financial mix? Here’s what you should know.

How does a high-yield savings account work?

This type of bank account is pretty similar to a regular savings account. You can use it to stash away money for an emergency fund or a big purchase, like a car or upcoming vacation.

Traditional and high-yield savings accounts share two more features:

- Your money could be insured. Check to see that the bank is a member of the Federal Deposit Insurance Corporation or National Credit Union Corporation

- As with a traditional savings account, you could be limited to six withdrawals per month

One key difference? With a high-yield account you typically get a higher interest rate than you would with a traditional savings account. As we mentioned above, that’s why these types of accounts are sometimes called high-interest savings accounts.

A quick refresher on interest: When it comes to savings accounts, interest is the amount of money you earn for leaving your money deposited with a bank.

When it comes to savings accounts, interest is the amount of money you earn for leaving your money deposited with a bank. It’s typically expressed as an annual percentage yield (APY), which is the amount of interest you could earn over a year, assuming that funds are not added or withdrawn.

APY accounts for compound interest, which is effectively making money on your money. The more often the interest compounds, the more money you could earn.

Compounding is important because the interest rate is applied to your balance, and the bigger the balance, the more interest you could earn.

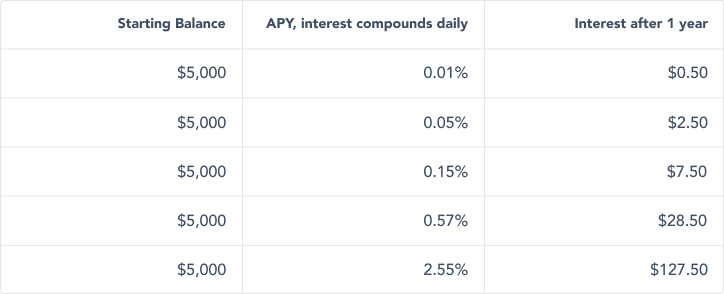

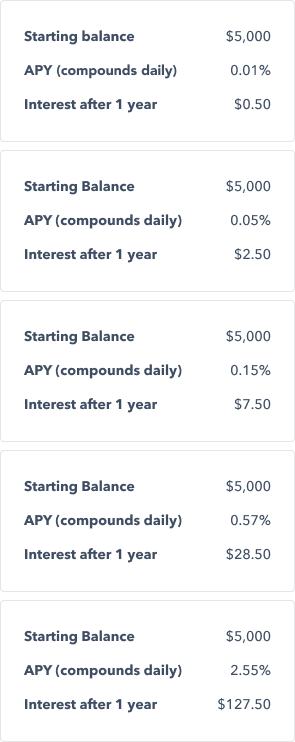

How much more interest could you earn?

The APYs on some savings accounts might not result in a lot of change to your balance. Check out this chart to see what we’re talking about.

How to choose the best high-yield savings account

You can open a high-interest savings account at a variety of financial institutions including online banks or at a credit union.

To choose the right account for you, it’s a good idea to do a little bit of research and comparison shopping.

Here are a few questions to consider:

- What is the interest rate? If you’ve been eyeballing savings accounts, you’ve might have seen both the interest rate and the APY listed; but the APY tells the fuller story . Some banks may also offer different APYs based on how much money you have in the account.

- How frequently does interest compound? Compounding is what turns a rate into a yield – it’s about how frequently the interest you earn in an account is added to your balance. Compounding is important because the interest rate is applied to your balance (principal and any interest earned), and the bigger the balance, the more interest you could earn. All things being equal, if one account compounds daily and one compounds monthly, why not make money on your money every day?

- Are there any minimum balance requirements or a required initial deposit? Some savings accounts require a minimum amount of money to open the account.

- Are there any fees? Fees are important to watch for because they could eat away at the interest you’re earning. For example, if your account has a $5 monthly maintenance fee, that’s $60 dollars you’re giving up every year. Some fees can be avoided if you meet certain requirements, e.g. keep a minimum balance each month .

- Do you have to open other accounts? Banks want more of your business. To get a better APY on a new savings account, some banks, for instance, may also require you to open a checking account.

- Is your account FDIC insured? This is an important thing to check off when vetting who you’re willing to give your money to. This page on FDIC insurance explains why.

Saving for the future starts today. See how Marcus can help.

How to open a high-yield-savings account

Found an account you like? Next step is to open it, which you can do in person or online depending on the bank.

The financial institution will usually ask you for a few pieces of information including:

- A driver’s license or passport

- Your social security number

- Primary bank information

If the account requires an initial deposit, you’ll need some funds to deposit into the new account. You can put in funds with cash, a check or wire transfer.

Once you’re done, you can start socking money away for your financial goals!

This article is for informational purposes only and is not a substitute for individualized professional advice. Individuals should consult their own tax advisor for matters specific to their own taxes and nothing communicated to you herein should be considered tax advice. This article was prepared by and approved by Marcus by Goldman Sachs, but does not reflect the institutional opinions of Goldman Sachs Bank USA, Goldman Sachs Group, Inc. or any of their affiliates, subsidiaries or division. Goldman Sachs Bank USA does not provide any financial, economic, legal, accounting, tax or other recommendation in this article. Information and opinions expressed in this article are as of the date of this material only and subject to change without notice. Information contained in this article does not constitute the provision of investment advice by Goldman Sachs Bank USA or any its affiliates. Neither Goldman Sachs Bank USA nor any of its affiliates makes any representations or warranties, express or implied, as to the accuracy or completeness of the statements or any information contained in this document and any liability therefore is expressly disclaimed.

Related Content

3 min read

3 min read

Connect with us on social media

Join our Marcus social media community, where we share content and inspiration to help improve your financial health. See you there!